Introduction

|

After 50 years of Philips Tuner development, we have reached the turn of the century, the year 2000. As described in Chapter 5, in the past decade the Philips Tuner business went through some fundamental changes. By 2000 the business was concentrated in two development centres, Krefeld (Germany) and Singapore, each with a volume production site in Kwidzyn (Poland) and Batam (Indonesia), respectively, while in Suzhou (China) production was ramping. More importantly, the last 10 years showed a major change in the product portfolio, moving away from TV tuners only. In several steps other RF applications were entered: satellite front ends and LNBs, multimedia frontends, communication modules and during the last years tuners for the new digital satellite and cable standards. In the classical TV tuner segment another dramatic change had happened, mainly due to the own initiative of the BU Tuners: the introduction of the WSP World Standard Pinning. This triggered a major change in the tuner market, one of the biggest being that the BU Tuners lost roughly 35% of its internal Philips TV volume. The more important second effect was a dramatic price erosion of the tuner function, being at only 3USD around the turn of the century. But, with the benefit of hindsight, we now know that these last ten years were quite calm compared to what would come next!

In this last chapter I will describe what happened in the turbulent last decade of the Philips TV, tuners and the associated semiconductor developments. Around the turn of the century the industry had reached the point where the centre of gravity of architectural ownership, cost and added value of consumer equipment shifted from the set (or module) maker to the semiconductor manufacturer. Although the semiconductor-driven integration was the engine of the continuous and spectacular price reduction of electronic equipment, it also changed traditional relations, focus areas of investment and management attention. But on the technology level major changes took place too, with unprecedented levels of integration and size reduction. These include the introduction of flat screen plasma and LCD TVs (plus the display technologies that did not make it), the change-over from analogue to digital TV, almost full integration of the TV processor, the Silicon Tuner, and all this in combination with price reductions to levels unheard of in the previous decades. New application segments were explored, like TV-on-Mobile, WiFi, GPS and even GSM, forcing the BL RF Solutions (as it became known throughout most of the period covered in this chapter) to adopt much more advanced packaging technologies. But then those applications allowed it to engage with leading players like Nokia, which in turn lead to the transfer to Philips Semiconductors, NXP and ultimately Nutune. And all this while volumes doubled to the unprecedented level of 50Mio modules by 2007, demanding enormous effort from the production organisation. In the background much bigger things determined developments at the level of the tuner business: where Philips had settled into a kind of stable mode with its Japanese competitors, now the Korean companies Samsung and LG came up aggressively, especially in the field of LCD TV. In parallel Philips tried to play in the emerging Silicon Valley biotope, until everybody was kicked out by the bursting internet bubble and dot-com crisis. And amidst all this Philips, Philips Consumer Electronics and Philips Semiconductors were struggling with the strategic questions how to cope with these challenges. Not surprisingly, it regularly resulted in major organizational changes, of which the tuner business was at best a part but often the victim. Ultimately it led to Philips selling off the business, be it TV, tuners, or semiconductors. Dramatic events ahead! |

Chapter navigation

|

Philips organization, 2000

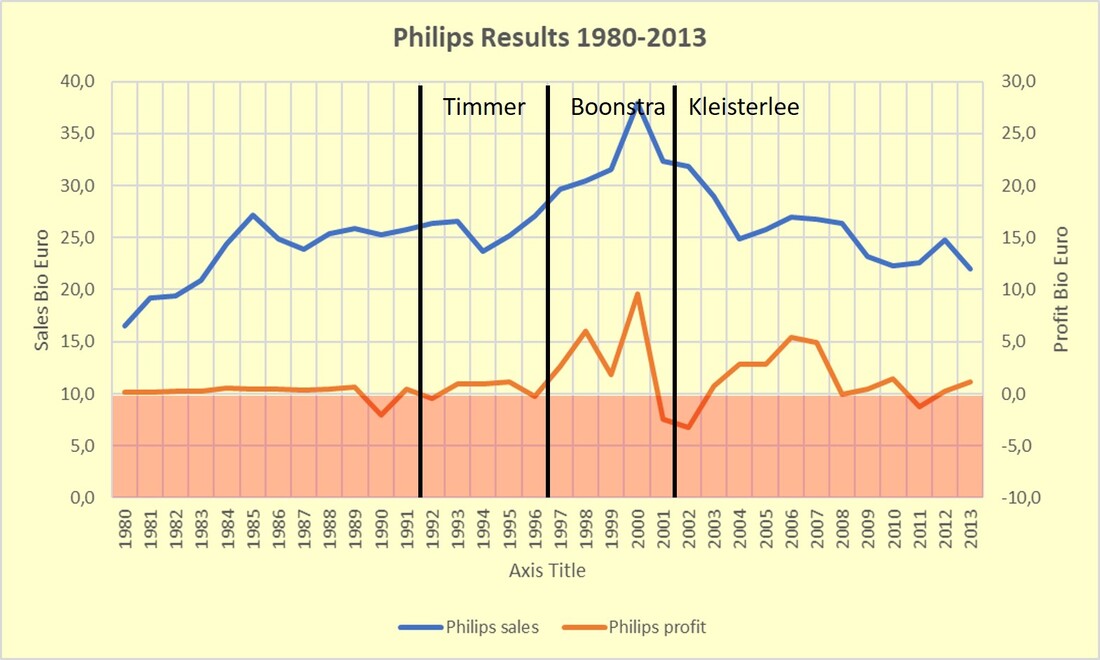

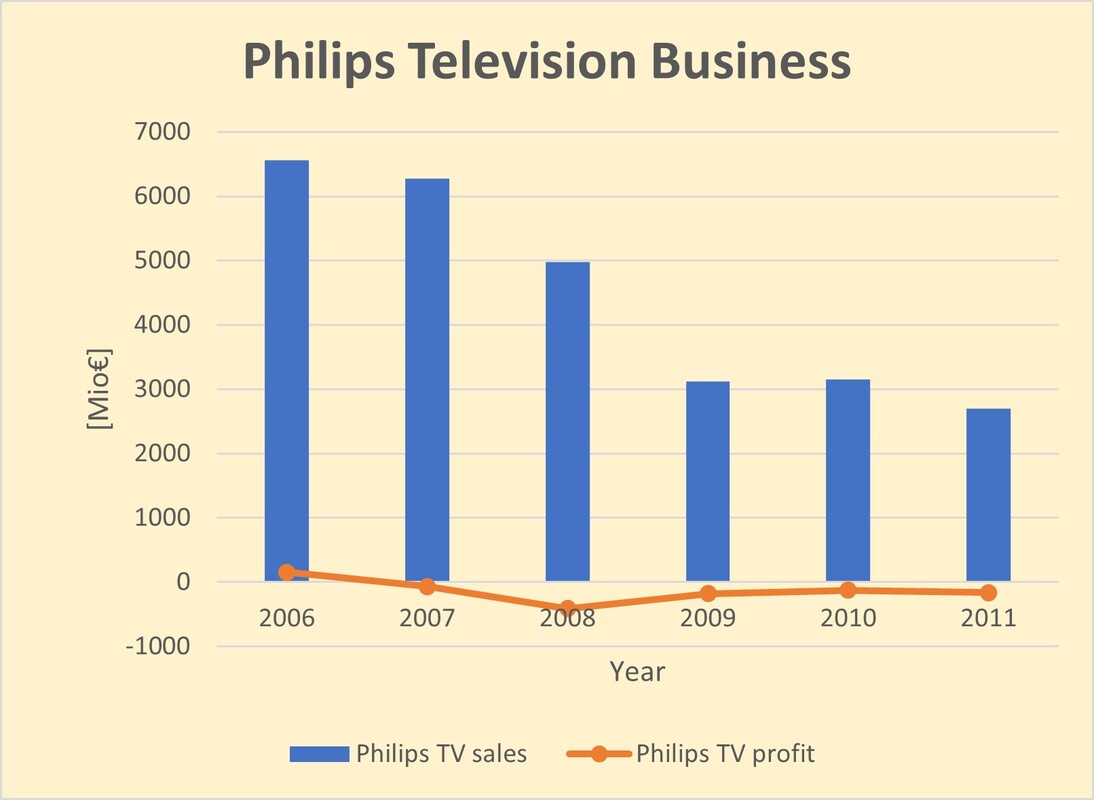

Philips entered the year 2000 still under the unpopular Cor Boonstra, who, in the past 5 years as president of the company, hadn't visibly learned anything about electronics nor about inspiring leadership. And nobody understood yet what he meant with his "Let's make things better" company slogan. In the meantime, many businesses had been sold or closed, but the backbone of the company remained the vertical integration of (from top to bottom) Consumer Electronics, Semiconductors and Components. Lighting, Domestic Appliances, Medical Systems and Business Electronics remained as cash generating units. The company still entertained 1800 people in Corporate Research. During a presentation for the Research management in 2000 Boonstra boasted that in the previous 5 years he had closed 5 divisions and 40 business lines. With the money from these sales and a relentless cost cutting programme Boonstra achieved a sales peak of 37,9Bio€ and a profit of 9,6Bio€ in the year 2000. Boonstra also had the tendency to alienate the management members around him, e.g. Jan Tollenaar of Sound & Vision resigned angrily, while hiring strange short-lived managers like Roel Pieper as CTO and intended successor of Boonstra. He survived barely one year due to conflicts of interest and was replaced by Ad Huijser, former head of TV development and recently head of Corporate Research. In 1999 two acquisitions were made: the US company VLSI was purchased for 1BioUSD, while Philips obtained a controlling share in LG Displays for 1,5BioUSD. However, Boonstra was the champion of short-term capitalism in its worst form, and in 2001 and 2002 with the internet-bubble burst, sales collapsed by 15% to 32Bio€, while profits turned into a loss of 2,5Bio€. That cost him the last support of the Philips Board, and he was forced to resign towards the end of the year 2001, only to get involved in formal lawsuits for insider trading in and around the company of his mistress. He was acquitted due to a lack of formal evidence.

|

Boonstra was replaced by Gerard Kleisterlee, in contrast to the outsider that Boonstra always remained, a manager that had grown through the internal ranks of Philips Components, of which he had become the division head in 1999. Kleisterlee was definitely a different personality from Boonstra, much quieter, no bluff, no boasting, but also not a great inspirational communicator. He acted more as a book-keeper and was extremely risk-avoiding and allergic to unexpected developments, especially those related to the financial predictability. As a result, he obviously disliked the marginal profits of Consumer Electronics as well as the cyclicity of the Semiconductor business. The main strategy of Kleisterlee and his management therefore became maximum financial predictability and minimal share price variations. Consequently, the focus of the company started to shift from the vertically integrated consumer electronics to medical systems, which up to then had been one of the modest and unspectacular professional business segments within the company. The fact that it did not grow, had highly predictable income due to contracts with hospitals and solid margins, now made it the heart of the company in the eyes of Kleisterlee.

|

Sales and profit history of Philips. The precidencies of Timmer, Boonstra and Kleisterlee are indicated. After the inflated sales peak in 2000 the decline is obvious.

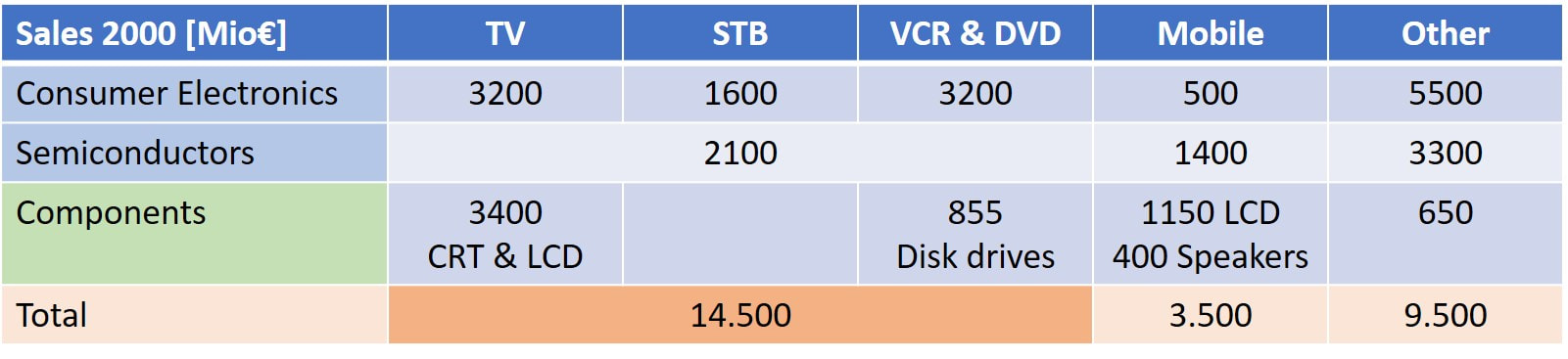

Rough split-up of the sales in the consumer pillar in the year 2000. Of the 38Bio€ company sales still 28Bio€ came from these businesses.

|

Philips president Gerard Kleisterlee. [Philips Annual Report 2004]

Philips CTO Ad Huijser.

|

The first victim of this new strategy was Kleisterlee's former PD Components. After he became the president of Philips, the Components division was taken over by Matt Medeiros, an American from Silicon Valley who, like most Americans at the time, believed the only place where one could develop new products was Silicon Valley. The headquarters of the Division were therefore moved from Eindhoven to Sunnyvale, and a major development site was created. At the same time Philips Semiconductors, for the same reason, was building up a massive organisation for developing CDMA-based 3G mobile phone ICs in nearby San José. The bulk of the Components business was still Display Components, by now a mix of CRT and - through the LG Joint Venture - LCD. Next to this, Components was market leader with black-and-white LCD displays for mobile phone applications, with Nokia as leading customer, while the new Liquid Crystal on Silicon (LCoS) technology was in development. Then, in 2001, the rapidly declining CRT Display business, with all its factories, was put into a joint venture with LG from Korea. This new entity named LG.Philips Displays was formally based in Hong Kong. This took the heart out of the division, which furthermore showed a 45% sales drop in 2001. This, in combination with the excessive costs of the Sunnyvale organisation, lead to the division Components being dissolved per January 1st, 2003. Matt Medeiros was fired, and the remaining activities spread across the other divisions. It also brought an end to the Silicon Valley presence of Philips, reducing it to a skeleton Semiconductor activity. As we will see, these developments also had major effects on the Tuner organisation!

|

|

Another development that was taking place within Philips, and especially Consumer Electronics, was the harmonization of the PCB manufacturing processes. This started around 1995 with project Lightning Stroke, a heavy top-down program that forced all units within Consumer Electronics to converge their PCB design of a limited set of 5 types, defining PCB material, thickness, metallization, number of layers, wired vs. SMD components, solder design rules, etcetera. The target was to harmonize all PCB stuffing and soldering processes, to create bigger factories that could serve multiple businesses with minimal process variation. This covered major factories of BGTV (Brugge, Dreux, Kwidzyn, Singapore, Manaus, Pune) but also VCR/DVD (Szekesfehervar, Hungary) and Audio PCB factories, in total nine. Around 1999 all these industrial activities were taken out of Consumer Electronics and concentrated in a new Philips Contract Manufacturing Services (PCMS). A last step was that, in 2002, PCMS was sold for 231Mio$ to the US EMS company Jabil. Only the final set assembly was now left within Philips.

|

October 2004 the Philips Board of Management unveiled the new company slogan "Sense and Simplicity", replacing the horrible "Let's make things better". It was on a big floating box in the Amsterdam canals.

|

Philips Tuners and RF Solutions organization, 2000-2006

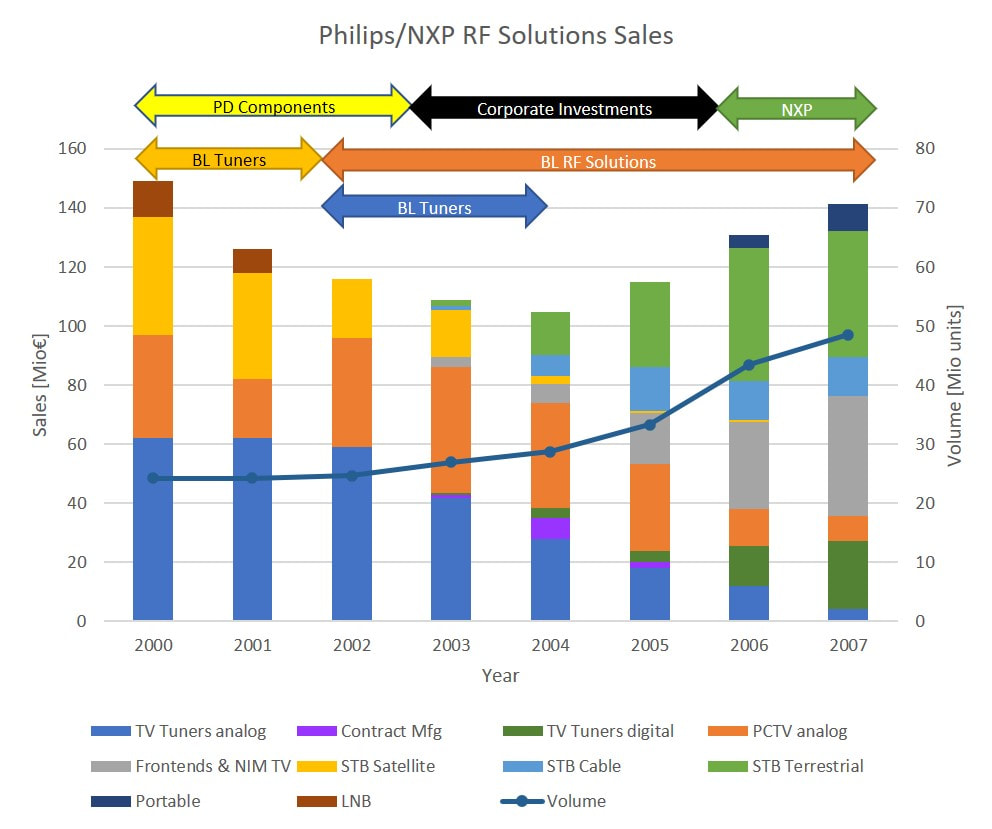

It can not be denied that at the turn of the century the BU Tuners was in a bad shape. As shown in the previous chapter, after an initial surge in sales to 240MioUSD in 1995, under the pressure of WSP price erosion this number had declined to a 10-year low of 125MioUSD by 1999. BU manager Rob de Ridder was promoted away to BGTV Operations, and after an interim period, was succeeded by Noud de Loos, the former manager of the Thick Film business in Krefeld. He had the difficult task to turn around the business in a very uncertain time. A good thing was that he installed three business segments with a certain degree of freedom to operate in their domain: Tuners, Multimedia and Set Top Boxes. This immediately gave more balance and focus. Already in 1999, triggered by the bad results, discussions started at company level what to do with the Tuner business. With de Ridder gone, the BGTV probably thought they has squeezed the maximum profit out of the BU Tuners, and it was no longer interested to keep the tuner business. There were serious thoughts to sell the entire BU Tuners. On the request of Ad Huijser, my former functional boss in BGTV and then head of Philips Research, I was asked to explain the importance of the RF competence and the opportunities of RF applications to the head of PD Components Gerard Kleisterlee and his CTO Marino Carasso. This was just before Christmas 1999, and on June 29 the next year it was announced that the BU Tuners would move to the PD Components. I hope my explanations have helped to come to this decision (although they never tell you). The same happened in parallel to the Remote Control Business. Both Tuners and Remote Control, now Business Lines, ended up in the BU Advanced Ceramics and Modules (ACM), which had as main business the ceramic Surface Mounted Components (SMD resistors and capacitors) in Roermond, the Netherlands. This BU had ambitions for increased RF activities using their ceramic substrate technologies. However, before the Tuners had landed within ACM it was announced that the SMD business was sold per July 1st, leaving behind a much smaller BU ACM.

A typical Philips MMRadiolink microwave product: a 27-28GHz microwave radio link transceiver.

|

As already explained, the PD Components was not a stable nor quiet location, with overall a dramatic collapse of sales due to the bursting internet bubble in combination with the rapid decline of CRT displays. A continuous portfolio analysis was taking place, where the first victims were the two microwave activities: Hazel Grove (Manchester, UK) and Krefeld. In 1999 the first, Philips Broadband Networks, was moved into Corporate Redesign, the organizational basket containing all business going through a complete redesign or being prepared for sale. With this group the BU Tuners LNB group in Krefeld had jointly developed the 28 and 42GHz MVDS modules. Initially it was thought this activity had a bright future, and a heavy investment had brought it from 30 to more than 100 people. It was re-baptized into MM-Radiolink in the process. However, towards 2001 it was concluded that the future was not as bright as hoped for, sales was only 4Mio€ and the unit was made ready for sale.

|

The same happened to the Krefeld LNB business, which was larger at 12Mio€ sales, but this was 50% below budget because also the LNB market saw an enormous crunch. On June 1st, 2001 it was announced that both MMRadiolink and the LNB business were for sale. The LNB business was eventually sold to Newtech (Belgium) in March 2002, but the MMRadiolink organisation was closed. Newtech could use the Philips brand name for another two years, but quickly changed to the brand Skyware. Ironically, by that time the LNB production, which had used sub-contractors for everything but the PCB stuffing P1, was concentrated completely in Krefeld. It used fully automated production lines with only two operators, one at each end. All other manufacturing of the the BU Tuners had moved out of Krefeld to Kwidzyn (Poland) or Asia. So with this move, Philips lost its very last manufacturing operation in the once enormous Krefeld TV/VCR/Tuner factory.

The fully automated LNB production line in Krefeld. The pink covers belong to the FCM component placement machines, behind them the reflow ovens. [Leaflet Skyware LNBs, 2002]

|

The same production line from the other side. note that only half of the hall is used. [idem]

|

As explained in the previous section, in the meantime the PD Components headquarters had moved to Sunnyvale, the focus was on supposedly rapidly growing emerging segments around wireless connectivity, and loss-making units in older segments were analysed for their strategic future. Including Tuners, because 2001 was a bad year with 8% negative Income from Operations (IFO). Tuners was now part of the renamed BU Emerging Electronic Systems (EES) which also contained Remote Control, Speaker Systems and Wireless Connectivity. The strategy department of Components started an analysis of the Tuners business and concluded it should be driven in a different direction. To start with, in November 2001 Noud de Loos was replaced by Pieter Paumen from the mentioned Strategy Department, and the BL received a new name to symbolise the fresh start: RF Solutions. But there was more, the BL was split into two separate business entities:

- BL Tuners, based in Singapore, would focus on the standard TV tuner (and the remaining TP900 VCR modules), and keep the Batam and Suzhou factories. Essentially this meant all liabilities were put into this BL: the rapidly declining tuner sales due to the WSP price erosion, and the Batam fab with its more than 1000 employees. The BL was assumed to remain profitable by doing contract manufacturing, first for the BL RF Solutions, but also for third parties. It was led by K T Goh, since 1996 the plant manager of Tuners Singapore. In total 169 non-production people (in Philiops terminology "indirects"), which included some 25 R&D personnel.

- Manufacturing activities in Singapore were stopped almost completely, all P2 (component stuffing) and P3 (alignment and test) moving to Batam and Suzhou. Only a prototype line remained and for a while the P1 (SMD placement) but also these would move to Batam soon.

- BL RF Solutions, based in Eindhoven, would take over development and sales - but not production - of all multimedia, satellite, and digital transmission modules. RF Solutions would buy manufacturing services from BL Tuners and thus became a fab-less business. It kept some 27 fte development staff in Krefeld and took over 18 R&D people in Singapore.

Driven by the vision of Rick Harwig, the new head of Research, from around 2000 the NatLab Research complex went through a massive transformation. On the one hand third party R&D activities were invited to the new complex, while in parallel all remaining Philips activities in Eindhoven were concentrated here. Many new buildings were erected, including large restaurant facilities along the pond, The Strip. It now houses around 12.000 employees.

|

In Singapore, Toa Payoh Philips still occupied its four former factories, although production quickly moved out. Tuners and RF Solutions remained in TP3, where a Medical Customer Training Centre occupied the former Tuners production floor.

|

But developments didn't end here. Having barely landed in the PD Components during 2002, both BLs were confronted with the dissolution of the PD by the end of the same year. The number of PDs interested in Tuner business was zero: Consumer Electronics had dumped them a year ago and Semiconductors was not interested in modules. Consequently, both BLs also ended up, together with quite a few other businesses, in Corporate Redesign, which had just sold off the LNB business. Having gone through the strategic analysis that lead to the split of RFS and Tuners, the obvious intention was to keep RF Solutions, which was deemed to be the promising growth part, and to get rid of Tuners with its manufacturing liabilities and diminishing margins. During 2003 several companies were approached for buying the BL Tuners, but eventually no deal was made. In fact, Corporate Redesign concluded that BL Tuners could not be sold stand-alone, but only in combination with something offering it a future: BL RF Solutions. And so, it was decided that per 1-1-2004 the two would merge again, becoming the new BL RF Solutions. With the clear intention to sell this business!

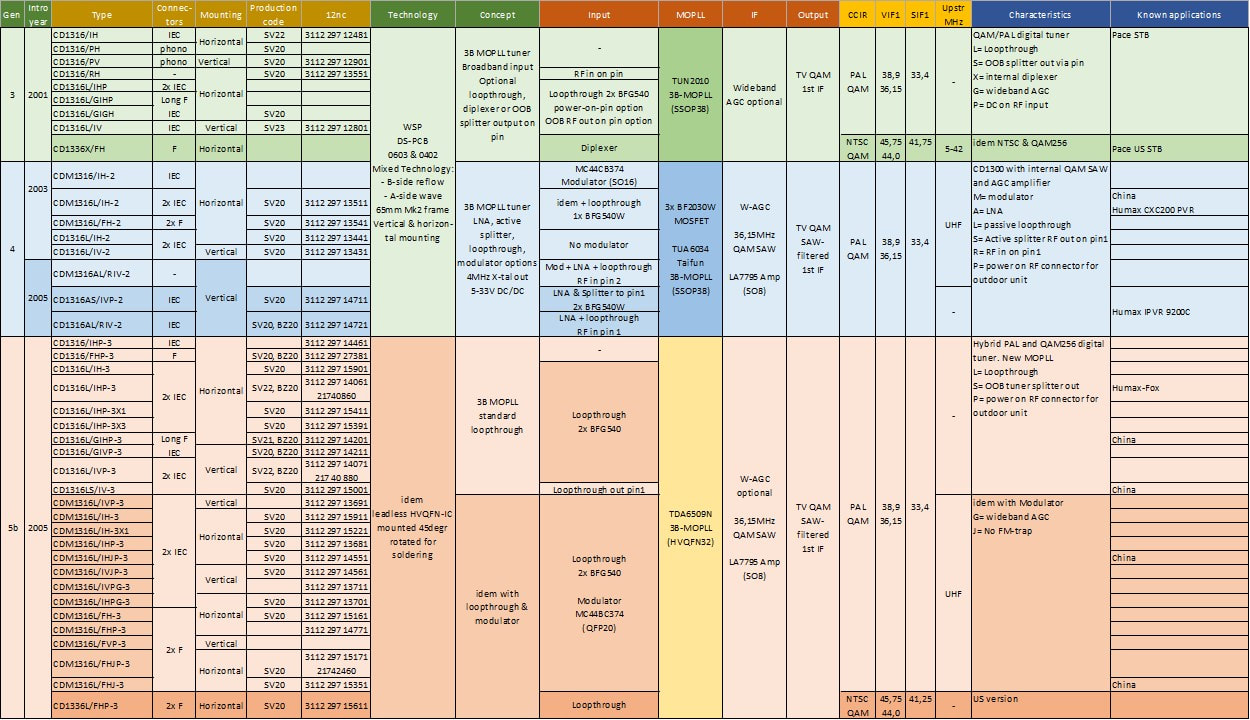

With all these strategic analyses and organizational changes, the portfolio split within the Tuner business became even more evident. On the one side were the good old TV tuners, and for a short while the dying TP900 tuner-modulators for VCR. Here price erosion continued in a devastating way, reducing the standard WSP tuner price from 3,4USD in 2000 to 1,99USD in 2005. Of course, this trend severely impacted the tuner supplier world, and especially the Japanese smaller players with their expensive cost base soon gave up: Hitachi, NEC, Sony and Sanyo. Although the Philips tuner volumes remained high throughout this period (around 17-18Mio pcs/year), the company was not able to grab additional volume due to this consolidation, mainly because new Chinese and Korean players stepped in with even lower prices. For Philips there was no way to compensate for this price erosion, so sales and margins declined continuously.

After the spin-off of the LNB business in 2002, there remained two dominant application clusters for RF Solutions: PC-Multimedia (PC-MM) and Set Top Box (STB). During the first years of the decade PC-MM, the FI/FM/FQ1200 family, was the cash generator of the BL, with a constant market share of 60-55%. This despite relatively very small investments, because for many years BU Strategy deemed it to be an unattractive market segment! Although the MM frontends were also used in the first small screen size LCD-TVs and monitors, the main issue was the lack of real market growth. TV on a PC remained a niche and was later replaced by video streaming.

The STB market was where the digital transition was taking place, first in Satellite, then Cable and ultimately Terrestrial reception. RF Solutions was an active player in all three of these segments, with all the positive and negative consequences: broad player, large experience, but many different products and impossible to focus. On top of that, typical for these type of system changes, the market and customers are uncertain and tend to watch competition before deciding, there are multiple scenarios that can be followed, with different (large) players following different scenarios, leading to different products for the same segment. In general, the BU followed the approach to have PC-MM products based on the 1200-family frames with Philips pinning, while STB products were all based on WSP, but this was only in theory, because especially the 1200-products were used in STB too.

In this chapter we will thus see many different product families:

After the spin-off of the LNB business in 2002, there remained two dominant application clusters for RF Solutions: PC-Multimedia (PC-MM) and Set Top Box (STB). During the first years of the decade PC-MM, the FI/FM/FQ1200 family, was the cash generator of the BL, with a constant market share of 60-55%. This despite relatively very small investments, because for many years BU Strategy deemed it to be an unattractive market segment! Although the MM frontends were also used in the first small screen size LCD-TVs and monitors, the main issue was the lack of real market growth. TV on a PC remained a niche and was later replaced by video streaming.

The STB market was where the digital transition was taking place, first in Satellite, then Cable and ultimately Terrestrial reception. RF Solutions was an active player in all three of these segments, with all the positive and negative consequences: broad player, large experience, but many different products and impossible to focus. On top of that, typical for these type of system changes, the market and customers are uncertain and tend to watch competition before deciding, there are multiple scenarios that can be followed, with different (large) players following different scenarios, leading to different products for the same segment. In general, the BU followed the approach to have PC-MM products based on the 1200-family frames with Philips pinning, while STB products were all based on WSP, but this was only in theory, because especially the 1200-products were used in STB too.

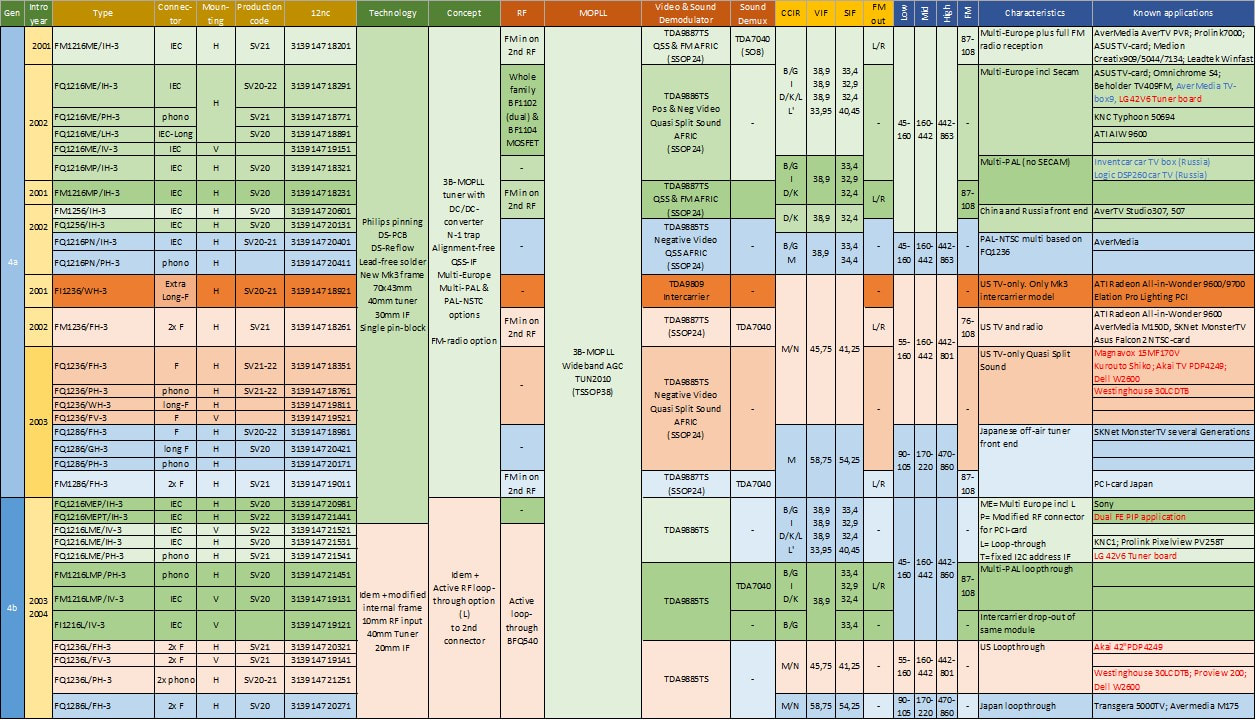

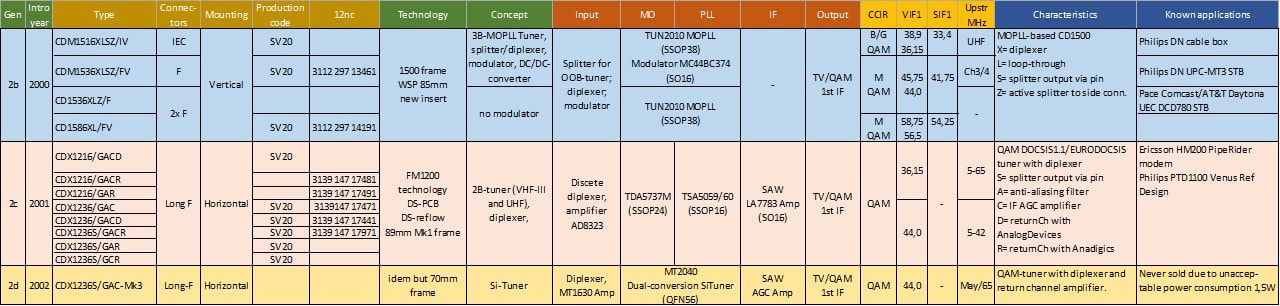

In this chapter we will thus see many different product families:

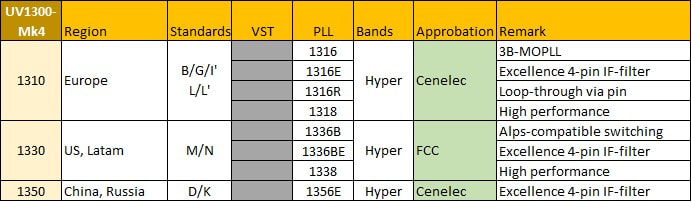

- Analogue tuners UV1300-Mk4, UV1300-Mk5

- Analogue MM-frontends FM/FQ1200-Mk3, FQ1200-Mk4, FQ1200-Mk5

- Hybrid MM-frontends FCV1200, FMD1200-Mk3, FQD1200-Mk5, FQD1100

- Terrestrial NIM TU(V)1200

- Terrestrial digital tuners TD1500, TD(M)1300-Mk1, TD1300-Mk2, TD1300-Mk3, TD11/1600, TD1700, HD1800

- Cable frontend CDM1500, PM1300, CDX1200, CD(M)1300, CD1600

- Cable NIM CU1200, CU1200-Mk3

- Satellite frontend SD1200-Mk3, SDM1700, SD1800

- Satellite NIM SU1200, SU1200-Mk2

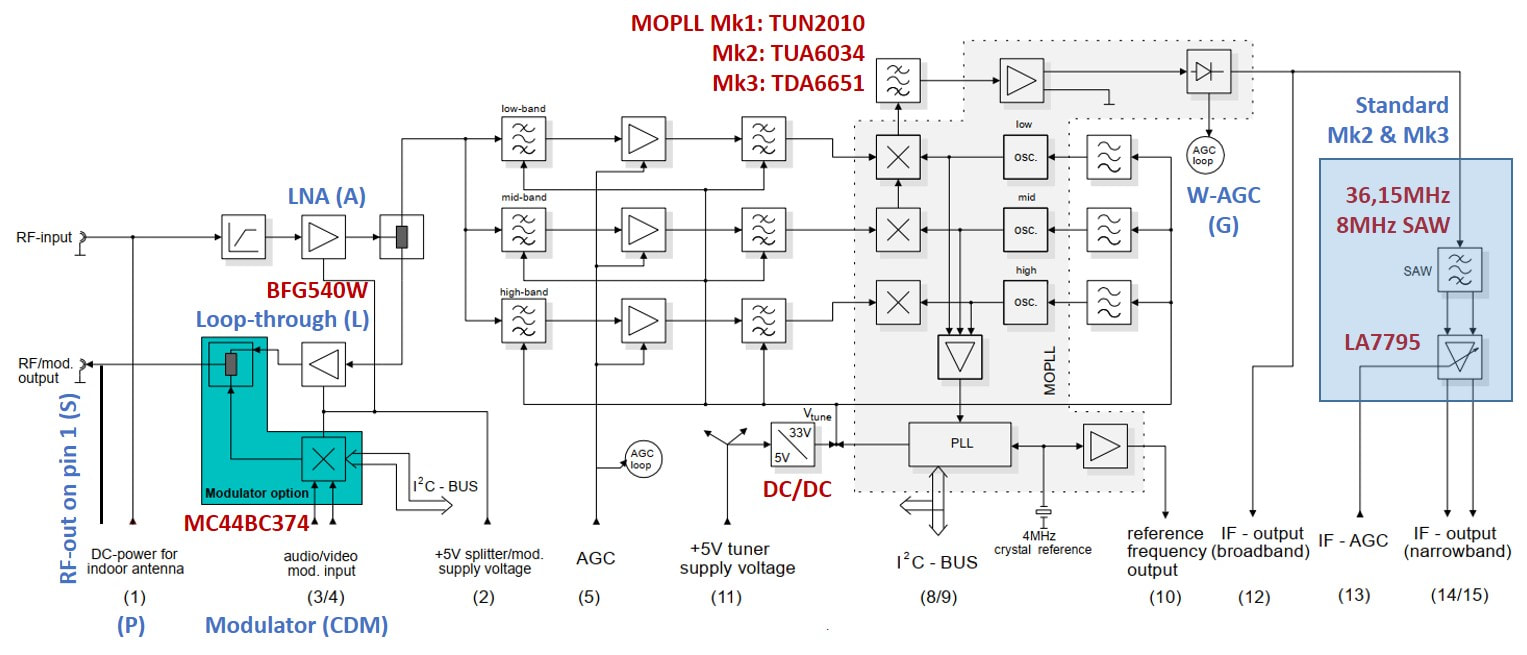

The NIMs mentioned in above list were the real new product concept of the BL: Network Interface Modules, the full RF, IF and digital channel decoding function in one module. In other words, RF-to-MPEG2 Transport Stream conversion. As introduced in the previous chapter the BU Tuners had experimented with these full conversion function in the QP1200 and QA900 products, but these were still using a tuner on a PCB. With the NIM it became all integrated on one PCB inside a single module.

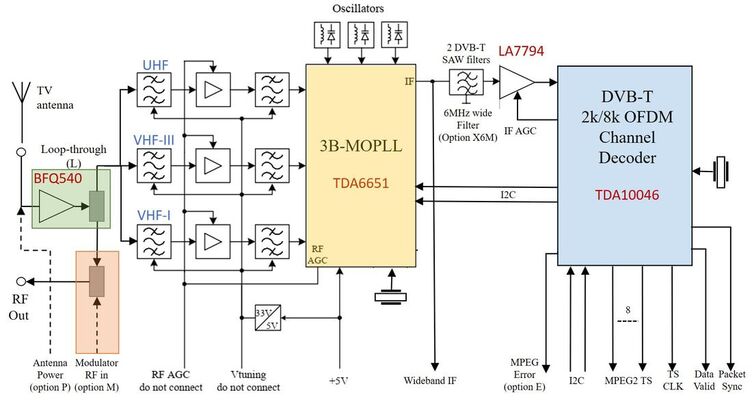

DVB-T OFDM, Digital terrestrial TV, 1997

In the previous chapter the first two digital broadcast standard were introduced: DVB-Satellite and DVB-Cable. The introduction of these standards was determined by the complexity of the modulation and demodulation, which is dependent upon the channel characteristics. Reception of geostationary satellites provides the most stable radio channel: very stable wide channels, only minor received power variations due to cloud and rain attenuation, but a low power budget due to the long distance. QPSK has therefore been selected, requiring the lowest Carrier-to-Noise Ratio (CNR) and thus most robust against received power reductions. No channel adaptation or equalization is required. The cable transmission channel, in contrast, is much more variable, especially the frequency-dependent transfer characteristic, which varies substantially due to reflections within the cable network. In the time domain this is equivalent to echoes. However, the cable network easily offers high SNR, so to squeeze sufficient bit rate into a standard 8, 7 or 6MHz TV channel the higher order 64-QAM and 256-QAM modulation scheme is used, in combination with equalizers in the receiver.

The spatial allocation of transmitter frequencies in traditional analogue TV broadcast (top) and a Single Frequency Network (bottom). [Wikipedia]

|

The ultimate target for Digital TV, however, was obviously digital terrestrial broadcast, given that some 70% of consumers watched terrestrial off-air broadcast. Of the three broadcast systems (off-air, cable and satellite) off-air clearly has the least well-defined radio channel: received signals can vary considerably in amplitude (the reason why tuner AGC has been such an important issue throughout this Tuner History), while multipath reception or frequency selective fading can lead to serious picture distortion. Similarly, reception of an unwanted signal at the same frequency also gives picture disturbance. In the world of analogue TV, the latter problem was solved through an internationally coordinated system of careful frequency planning and allocation, guaranteeing that transmitters with the same frequency were sufficiently far apart. One of the ambitions of the new DVB-Terrestrial (DVB-T) standard was thus to solve both the multipath as well as the frequency allocation problems. Ultimately DVB-T was designed to support Single Frequency Networks (SFN), all transmitting the same channel on the same frequency. Obviously, when a standard is performs well in an SFN it is also robust to echoes.

|

|

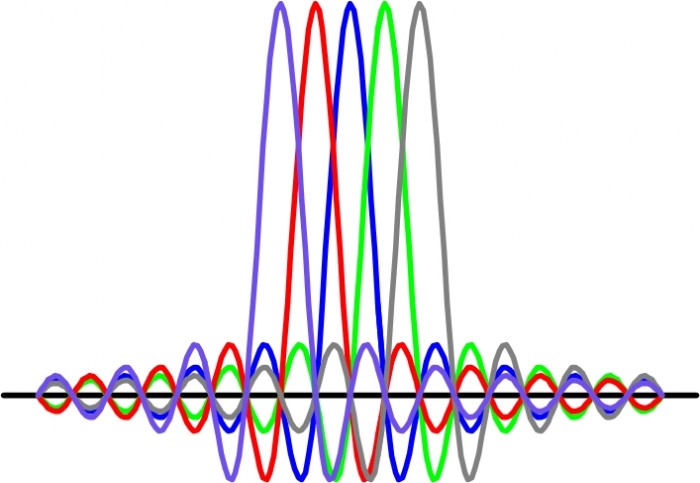

The technical solution to this challenge is Coded Orthogonal Frequency Division Multiplexing (COFDM, often shortened to OFDM). In QPSK and QAM the signal modulated on the RF carrier has the full symbol rate, thus occupying the full signal bandwidth and being sensitive to frequency selective fading, which in turn requires complex equalizers. In OFDM, in contrast, the incoming digital bitstream is split into many parallel symbol streams, each modulating a closely spaced frequency carrier. Using the proper relation between the individual carriers they become orthogonal, i.e. their frequency domain side lobes are zero at the centre frequencies of all adjacent carriers. In DVB-T either 1705 (2k) or 6817 (8k) carriers are used, which can be modulated individually using QPSK, 16-QAM or 64-QAM. Of course, a higher order modulation gives a higher bitrate and in practice 64-QAM is used. The distance between 2k-carriers is 4464Hz and for 8k 1116Hz, both fitting within an 8MHz channel (4464 * 1705 = 1116 * 6817 = 7,6MHz). Because all carriers are modulated equally the resulting frequency spectrum of an OFDM signal is almost perfectly flat, providing a very high bandwidth efficiency. To facilitate analysis of the effective frequency-dependent channel characteristic some 10% of the carriers is not used for data transmission but as fixed pilot, spaced evenly across the channel width and changing for every symbol. The strength of the pilots is used to estimate the Channel Transfer Function in the receiver, facilitating fast and adaptive equalization without complex computations.

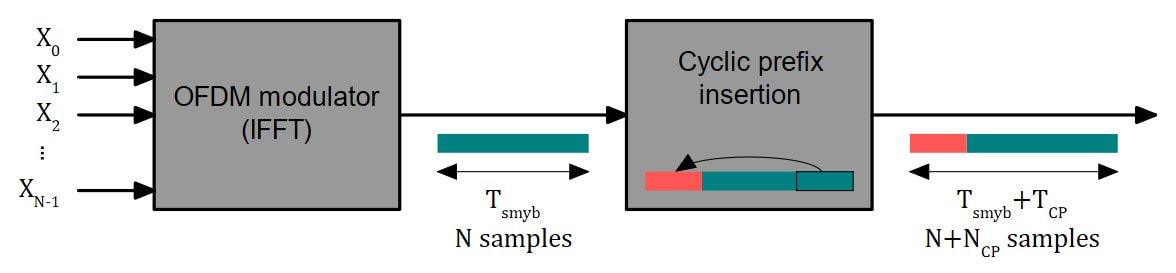

For transmission the so constructed frequency domain signal is translated to a time domain signal using an Inverse Fast Fourier Transform (IFFT). When the carrier distance is 1116Hz for an 8k system as given above, the symbol length Ts is 1/1116= 896us. An important characteristic of OFDM is now the guard interval or cyclic prefix, where a fraction 1/m of the first part of the symbol is repeated and added at the end, thus lengthening the symbol. The parameter m can be 32, 16, 8 or 4, lengthening the symbol to 924, 956, 1008 or 1120us. At the receiver these lengthened symbols allow the reception of delayed multi-path signals, the longer the guard interval, the larger the possible delay: for 2k and 1/32 the max delay is 7us equivalent to 2,1km, for 8k 1/4 it is 224us or 67,2km. Obviously, the longer the cyclic prefix, the lower the effective data throughput. |

Example of 5 orthogonal OFDM BPSK-modulated carriers. At the centre of a carrier all other signals are zero. [DSP-related.com]

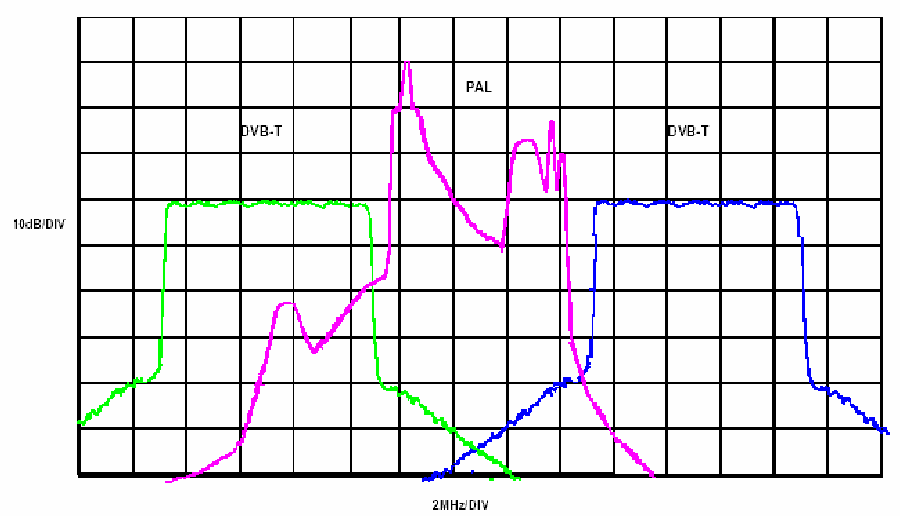

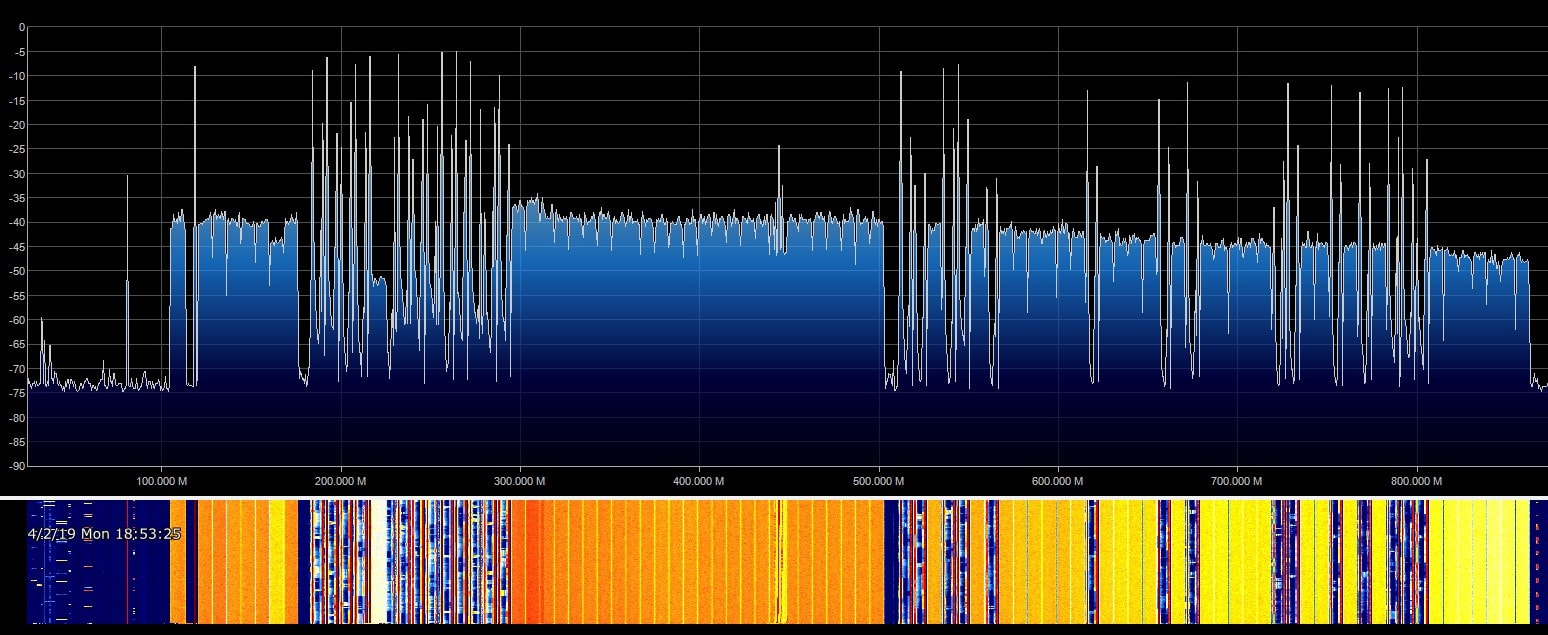

Spectral scan showing the clear differences in spectral density of a classical PAL TV signal (purple) and two adjacent OFDM signals. The situation shown (one PAL channel between two DVB-T channels) happens in practise and is the reason for stringent N+/-1 requirements. [SemanticScholar.org]

|

Concept of the cyclix prefix insertion in an OFDM transmitter. [Wikipedia]

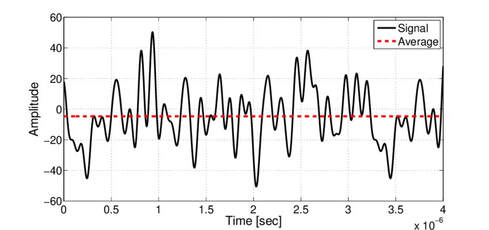

Typical OFDM time domain signal, showing the high PAPR. [Researchgate.net]

|

With these measures DVB-T is a system standard that is very robust against multi-path fading and/or variable frequency-dependent channel characteristics. The channel includes the receiver frontend part, and tuner tilt is thus no longer an issue for OFDM. In contrast, given the many carriers, LO frequency stability and phase noise are more critical, requiring large loop bandwidth PLLs. Furthermore, due to the statistically independent nature of the 2k or 8k orthogonal carriers they add non-coherently in the time domain, which means that the instantaneous signal amplitude can vary substantially. OFDM signals therefore have a high Peak-to-Average Power Ratio (PAPR) and need around 10dB back-off to avoid non-linear distortion.

And finally OFDM is very sensitive to (analogue) N+/-1 adjacent channel interference. For this there was no other solution than using two SAW filters in series, which in turn required additional IF amplifiers to compensate for the high SAW insertion losses. |

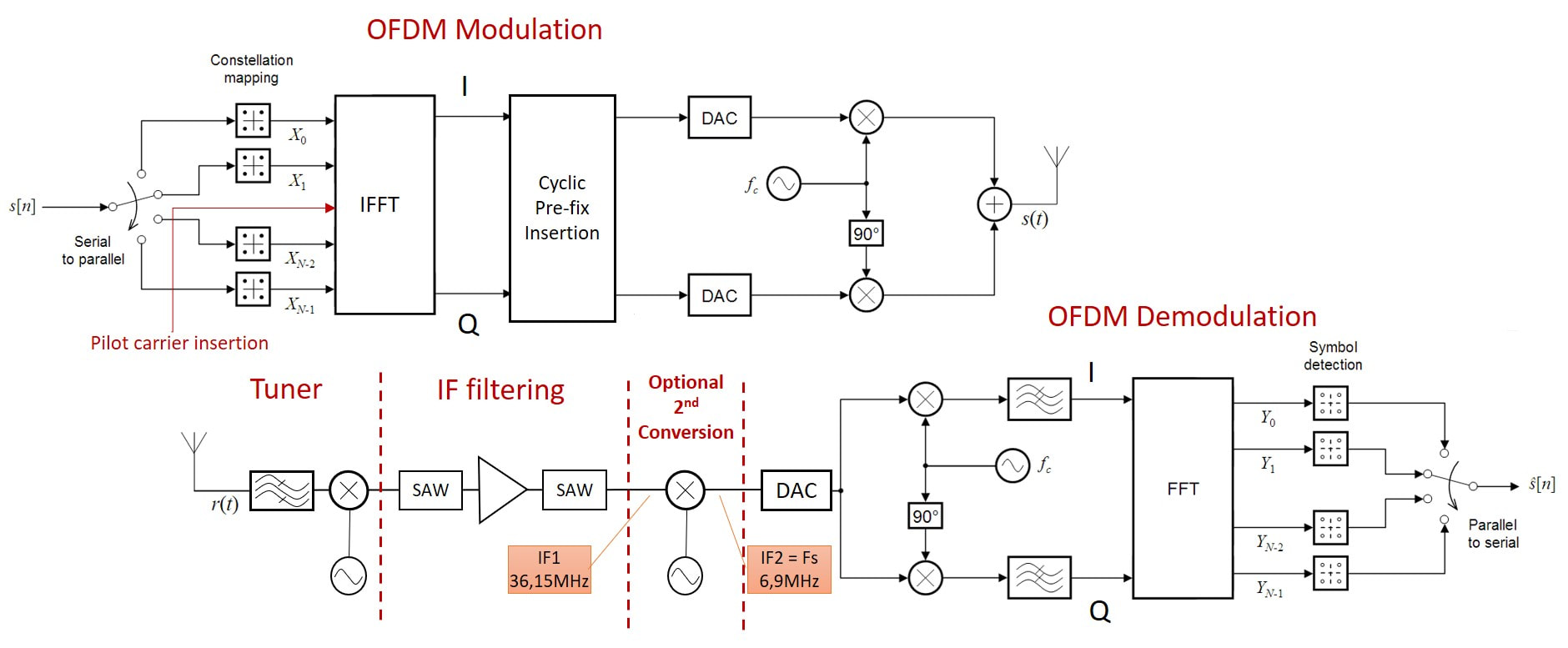

Typical architecture of an OFDM transmit-receive chain. The input and output are the coded MPEG2 streams. Because of the high adjacent channel rejection requirement most OFDM receivers required two SAW filters, with an additional amplifier to compensate for the losses. Early systems required a second down-conversion with IF2 equal to the symbol rate. [Modified from Wikipedia]

|

DVB-T is clearly a flexible standard, where operators can play with the system settings to optimize the quality and number of channels transmitted within one RF channel. For this they have the puncturing rate (1/2 to 7/8), the sub-carrier modulation format (QPSK, 16-QAM, 64-QAM) and the length of the cyclic prefix guard interval (1/4 to 1/32). Between the extreme settings this means the effective bitrate can be set between 5,0 and 31,7Mb/s, where the bitrate can be traded off against higher quality/resolution and higher multi-path robustness. To most operators the number of channels is most important, so typical bitrates are around 26Mb/s.

DVB-T was defined towards 1997, with first experimental transmissions from 1998 onwards in Singapore and the UK, and first formal introduction from 2001 onwards in the UK, Sweden, and Spain. Many countries followed. In the end all of Europe and 90% of Asia and Africa, except for Japan and China, converted to DVB-T over time. In Japan the Integrated Service Digital Broadcast - Terrestrial (ISDB-T) was adopted, also based on OFDM but now in 13 sub-channels, where single or combined channels can be QAM-modulated. In a slightly modified form this standard was also chosen by Brazil first and then the majority of South America. China developed its own DTV standard DTMB ten years later, allowing it to include more advanced signal processing features but still based on OFDM. It was introduced in 2006. Only the US ATSC system was different and will be discussed separately. |

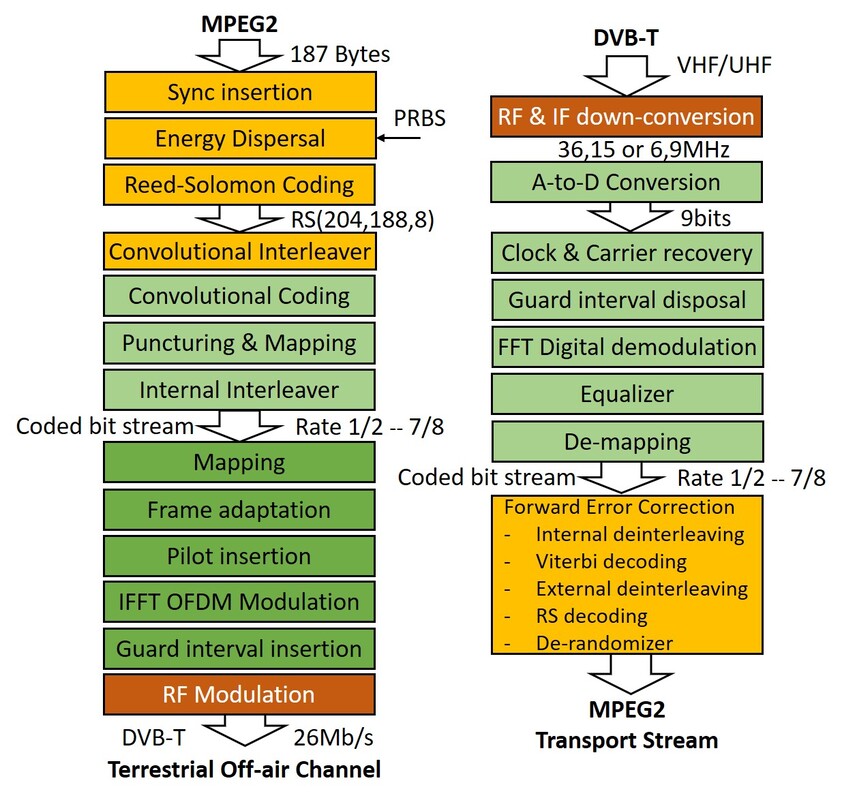

The full coding, modulation, demodulation and decoding chain of DVB-T. The encoding part up to the coded bit stream is almost identical to DVB-S.

|

Evidently all relevant Philips departments were involved with the early development and roll-out of DVB-T: Research in the standard setting, Digital Networks (Suresnes, Eindhoven) to develop the STBs, Philips Semiconductors for the ICs, and BU Tuners for the front ends.

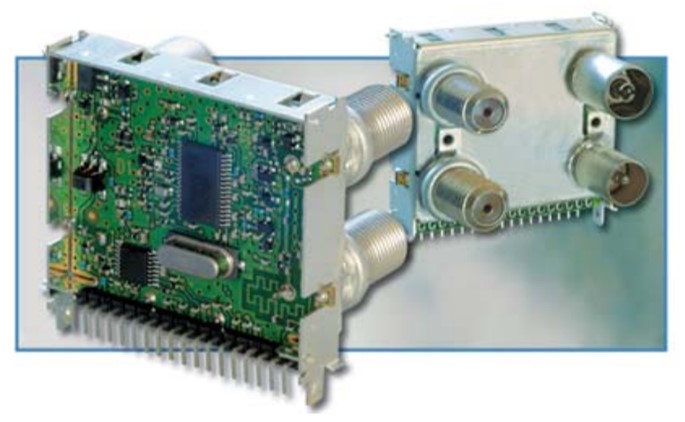

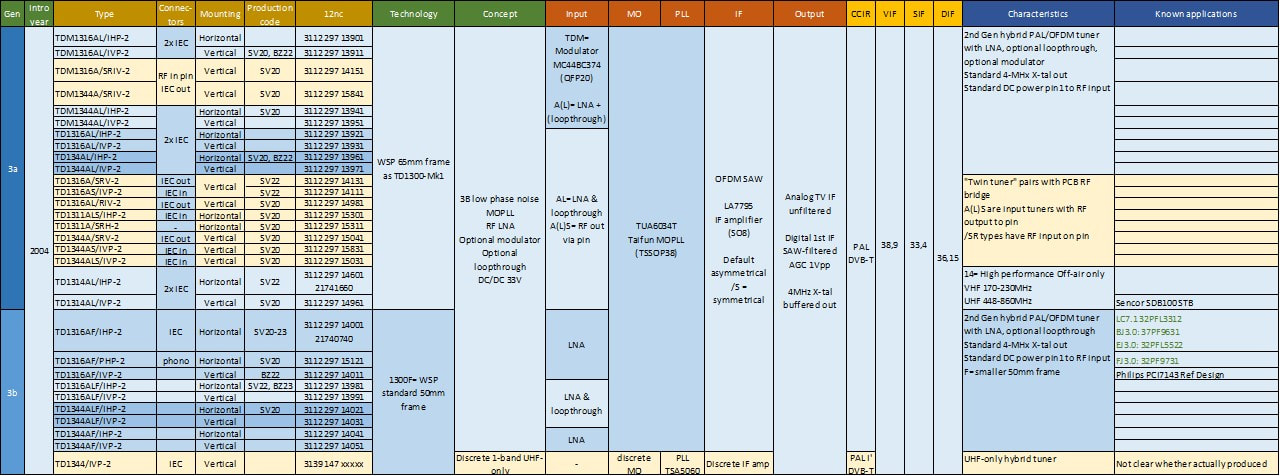

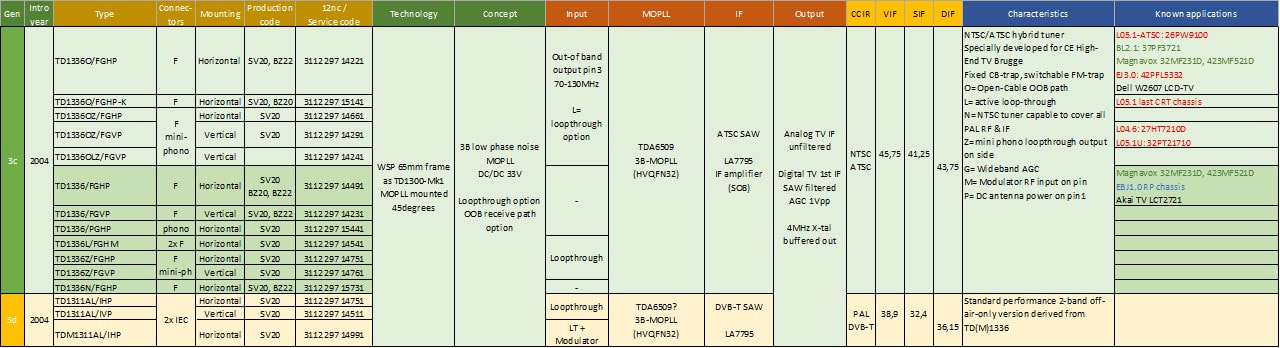

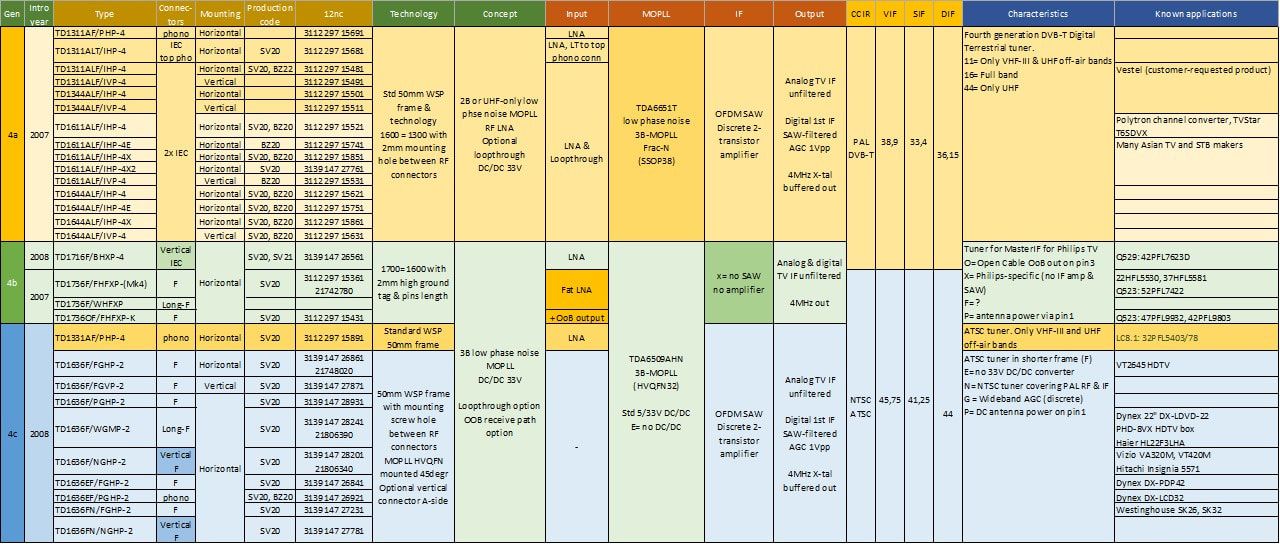

TD1500 and TDM1300, the first OFDM tuners, 1998-2003

The roll-out of DVB-S first and then DVB-C as described in the previous chapter happened within 2 years of the respective standards releases. This was possible because in both cases the receiver function was a Set Top Box (STB), in most cases provided by the operator. When a standard changed from analogue to digital the service provider would simply exchange the customer STB. The connection from the STB was preferably a new digital interface (HDMI), otherwise analogue (SCART) or worst case re-modulated on a carrier. In none of these cases the consumer needed to change its TV, assuming it had at least one of the mentioned interfaces. The DVB-T receiver was different and much more difficult because it was intended to replace the classical analogue TV tuner function. From the start there were at least two system challenges when introducing DVB-T in TV sets:

- how to provide both the new digital as well as the old analogue TV reception, which were to co-exist for at least another decade?

- what was the optimal system (read module) partitioning for OFDM reception?

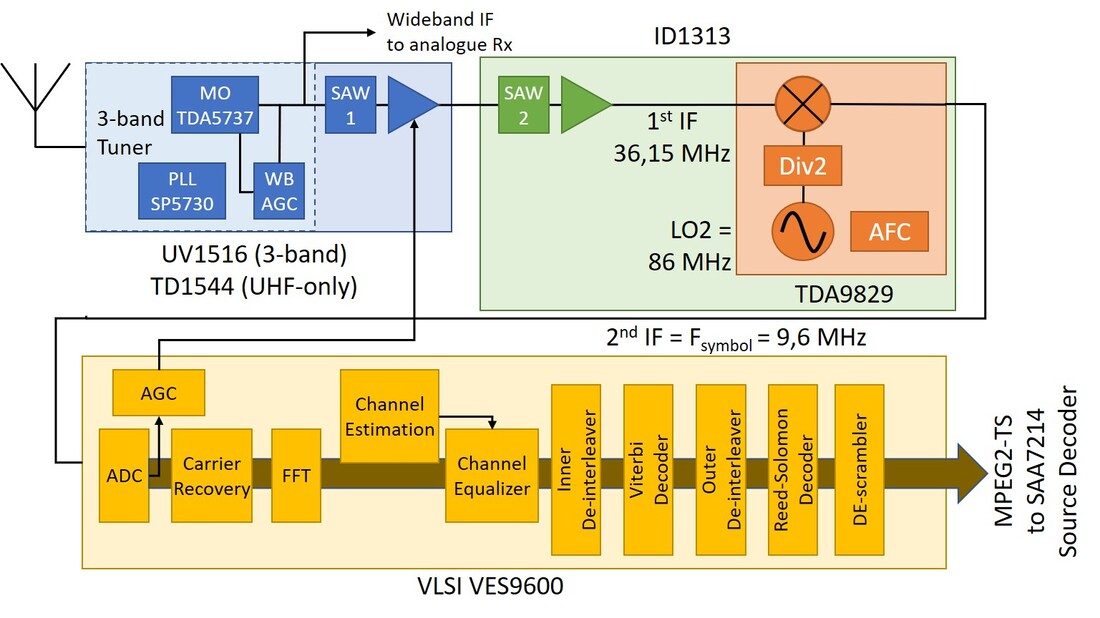

Block diagram of the digital channel section of the Philips IFA-1999 OFDM demo, which used the UHF-only TD1544. The ID1313 was an IF module containing the second SAW filter and amplifier. Although asked by some initial customers these modules were hardly ever actually sold.

|

The UV1516/I with the unique sliding cover, here shown when closed. The large dent in the cover is for ground contacting.

|

|

The first tuner for the OFDM application used the new 1500 WSP frame, introduced with the CD1516 cable tuner earlier the same year. In contrast to the the cable product, the OFDM tuner used the same tuner core for the analogue and digital reception and did not require a splitter or loop-through function. The uncertain times around the emerging DVB-T reception are illustrated by the fact that the first 3-band tuner was still called UV1516, while the UHF-only 1-band version became the TD1544, using the new product code TD for Terrestrial Digital. Because of the important off-air reception the TD1500 family featured the discrete Wideband AGC from the UV1316-Mk2 and the internal 5V-to-33V DC/DC converter from the FI/FM1200-Mk2. Interestingly, the most dominant European type in this initial phase was the UHF-only TD1544, still using the 3B-MO but with de-populated VHF bands. There were two reasons for this: the BBC was a leading partner in developing the first OFDM tuner since they were aggressively pushing DVB-T deployment in the UK to counter the success of Rupert Murdoch's BSkyB DVB-S satellite broadcast. At the same time, most initial DVB-T deployment plans in Europe (Sweden, Germany) focussed on the UHF only; only later would DVB-T be extended to the VHF-III.

|

Picture of the boards inside the BOCMA-based hybrid TV receiver as show at the IFA1999. On the lower right board are a CD1516 cable tuner and TD1544 OFDM tuner.

[Philips Semiconductors AN99061]

|

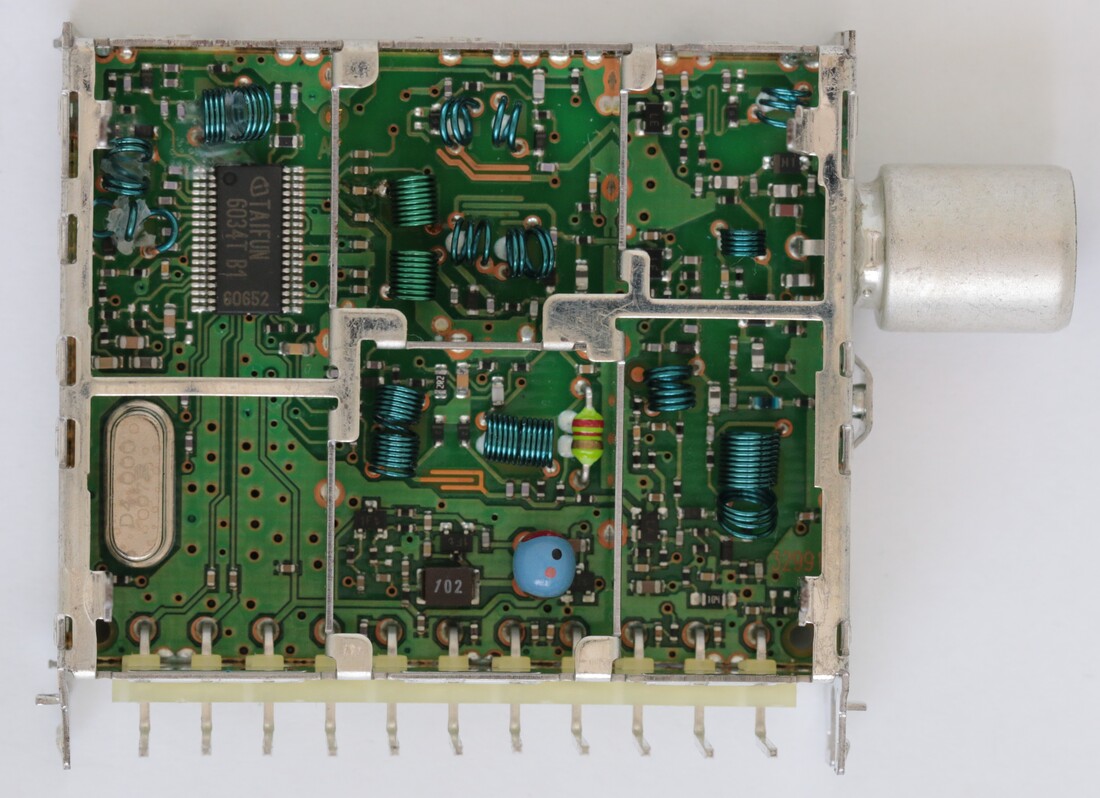

The Philips TD1544D/IH. On the right the dual input with at the bottom the DC/DC-converter. In the central section the empty VHF sections are visible. In the left section the OFDM BAW filter, discrete amplifier, W-AGC and the blue Sagami trafo for balanced IF output. Note that the low phase noise PLL is no longer from Plessey but Mitel. [via Darko Jancin]

|

It quickly became evident that the 1500-size tuners were too big, although they did provide good service during the early very low-volume days of OFDM introduction. A smaller module size was required, though, which was the 65mm WSP frame used for the UV1300A-Mk2. Compared to the now outdated TD1500 the TD1300 family introduced several new features:

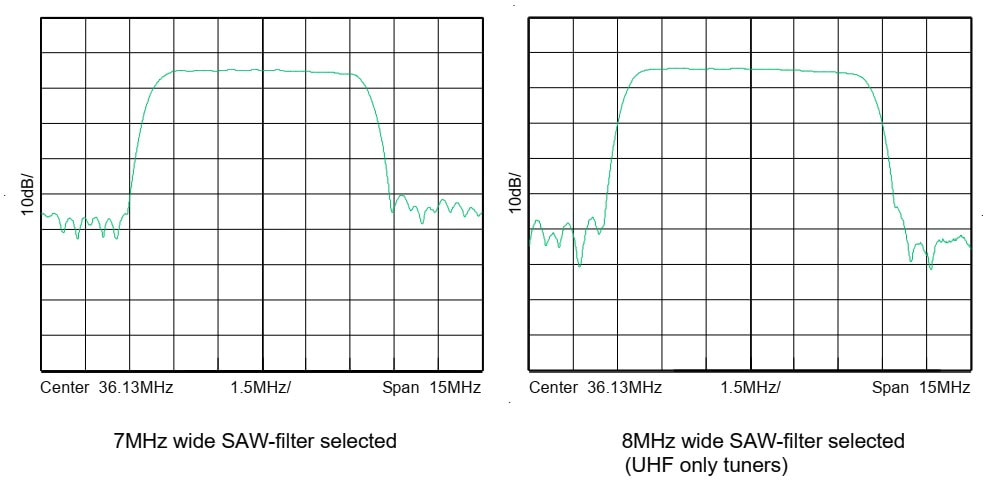

The switchable 7MHz (left) and 8MHz (right) SAW filters as measured inside the tuner. [Philips TD(M)1300AL Data Sheet]

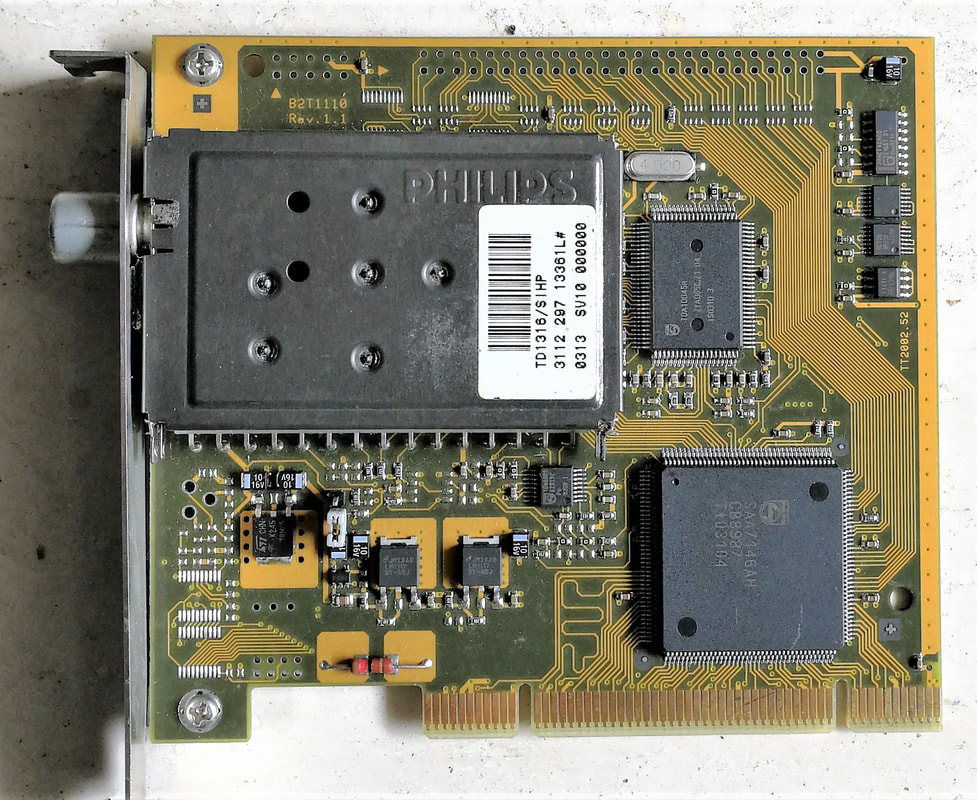

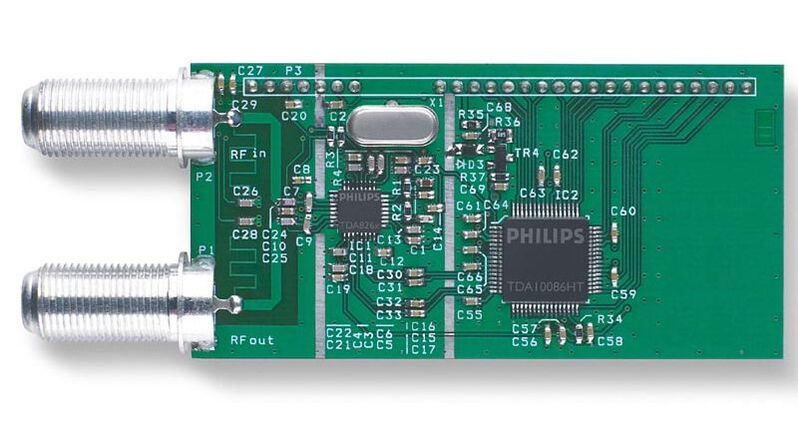

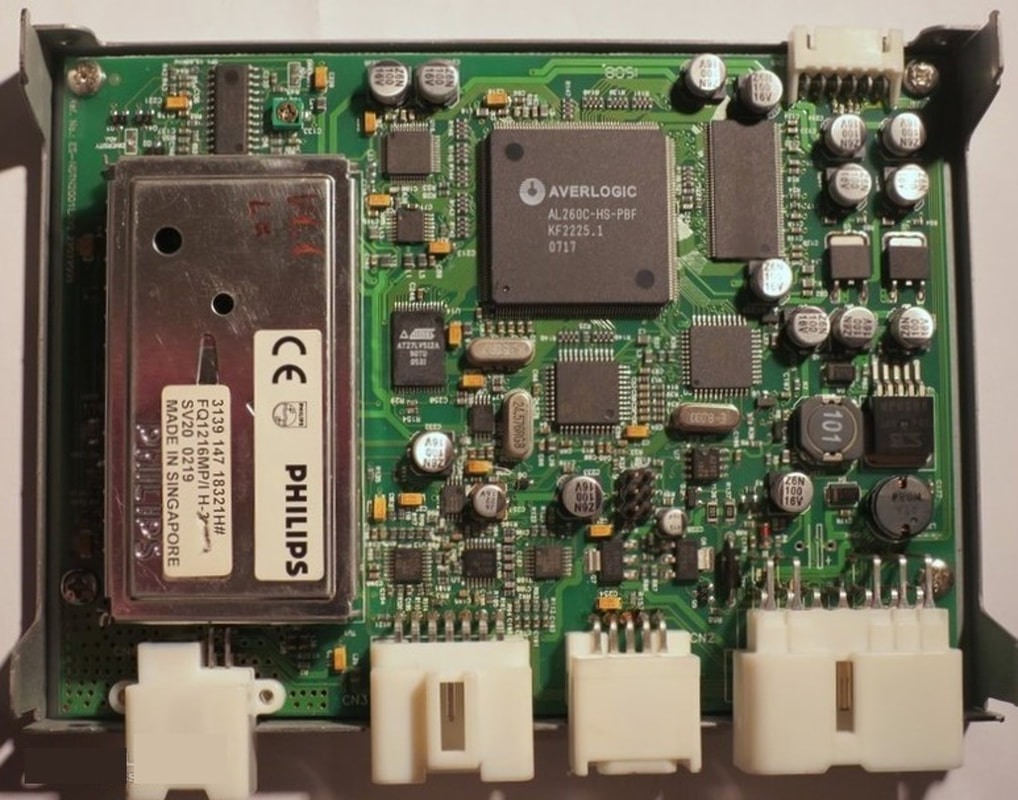

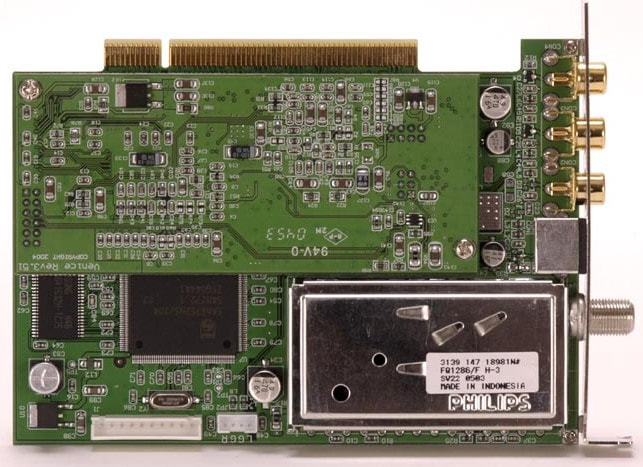

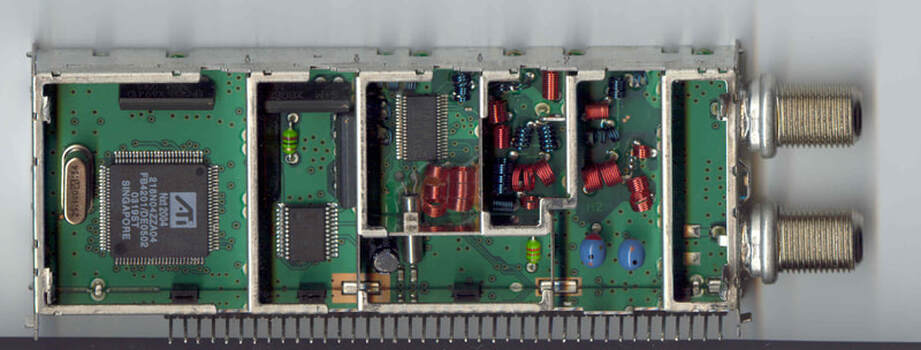

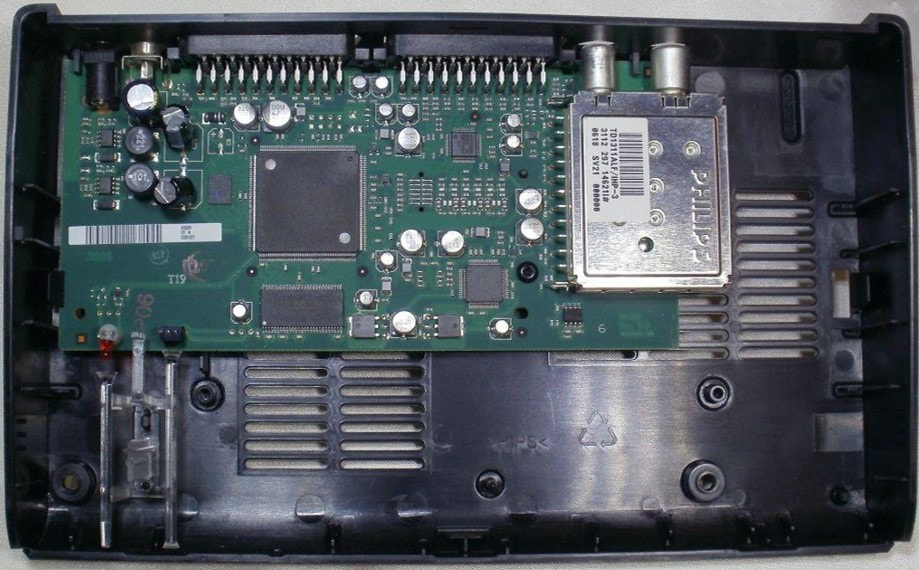

The new TD1316 on a typical PCI-card for digital TV reception on a PC. The two other large ICs are (top) the new TDA10045 OFDM channel decoder and (below) the SAA7143 source decoder and PCI bridge IC. Just below the tuner is the TDA9889 IF-to-low IF downconverter. [via Toh Kong Lim]

A second typical TD1300 application: DVB-T add-on boards for TV sets. Here the 2004 Intelligent Bolt-on (IBO) Zapper board of the LC4.3 LCD chassis 37PF5520. In the centre the Conditional Access (CA) card reader with STM card reader IC; right of this the QFP TDA10046 OFDM channel decoder. Upper left the PNX8316 Mojo MPEG2 decoder.

|

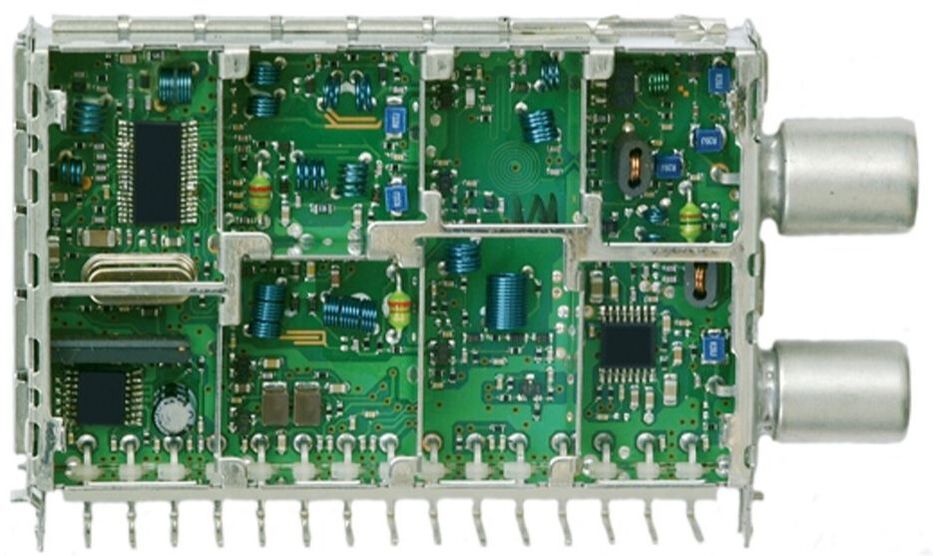

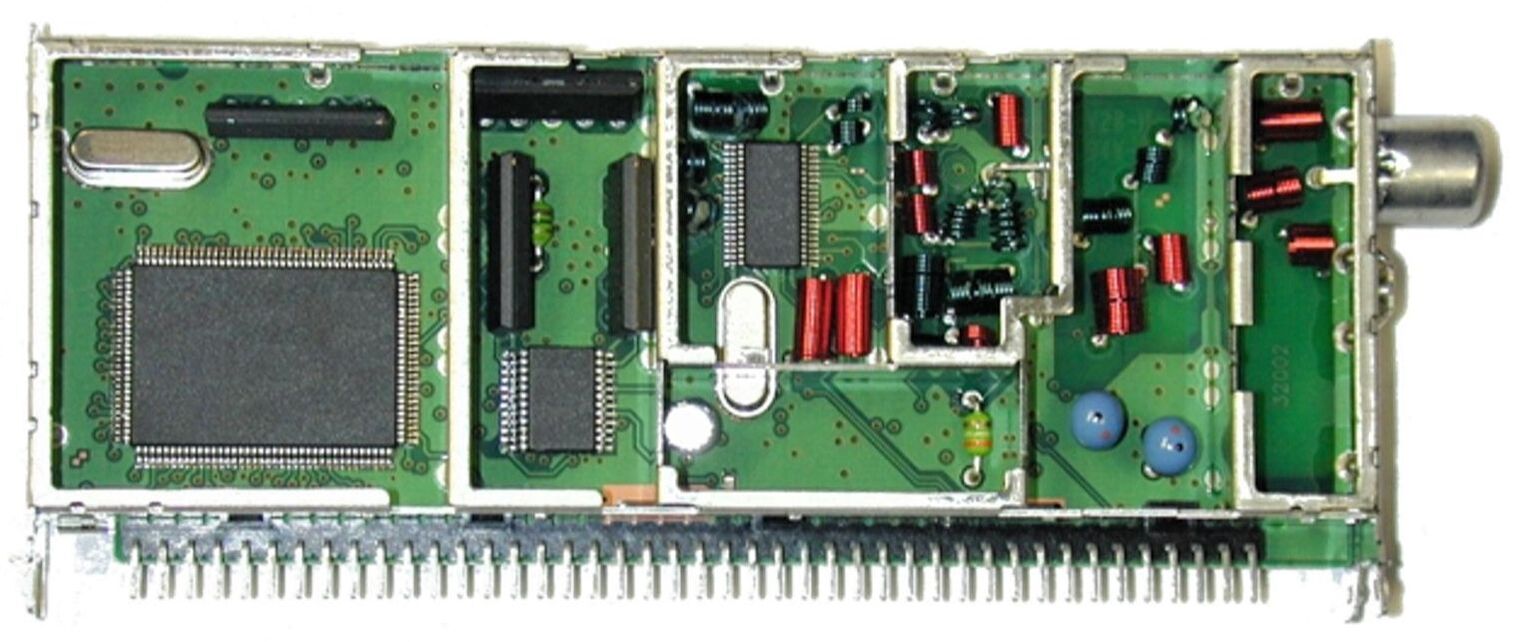

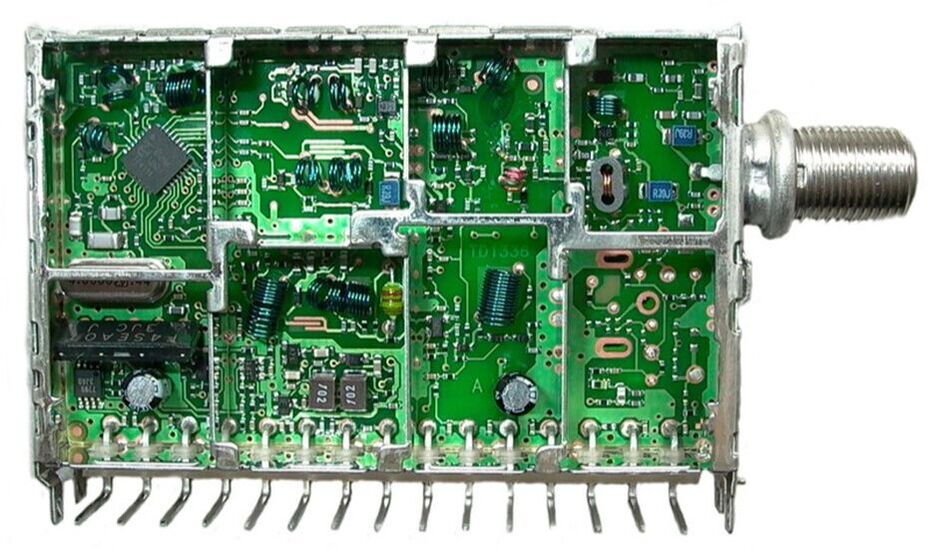

Interior view of the TD1316/SIHP. Upper left the MOPLL, lower right the empty slot for the modulator. Lower left the blue SAW filter and below it the Sanyo amplifier. The two grey blocks marked 102 belong to the DC/DC-converter. The type number suffixes SIHP refer to Symmetrical IF output, IEC, Horizontal mounting, and Power to RF input via pin1.

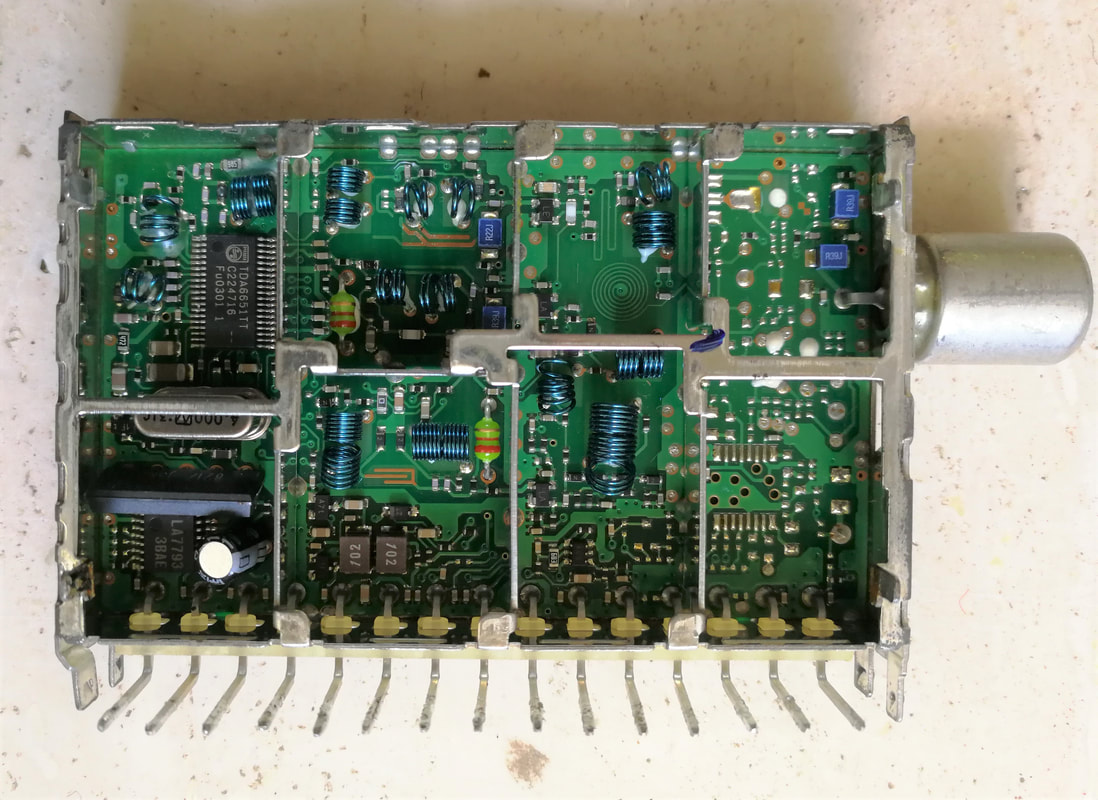

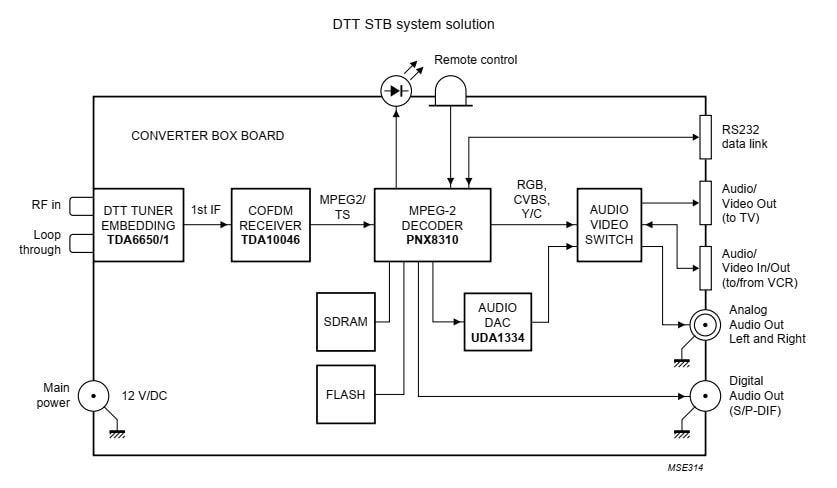

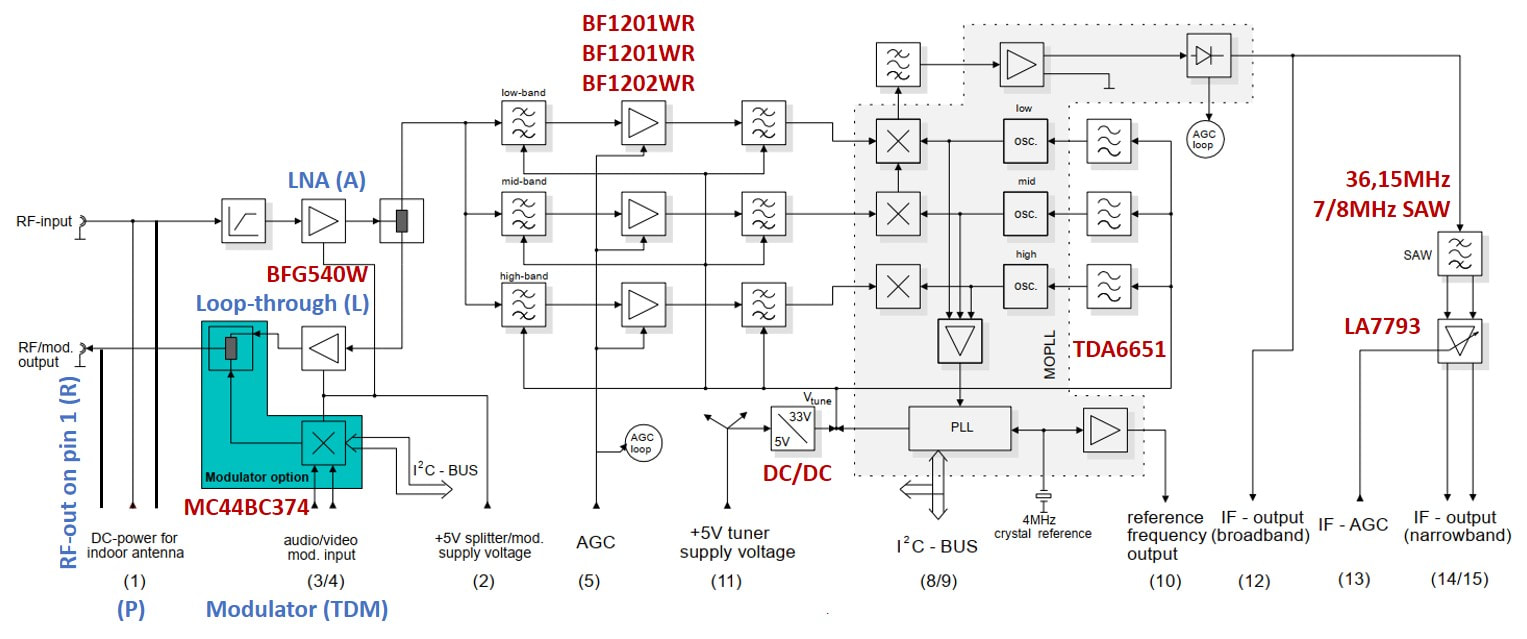

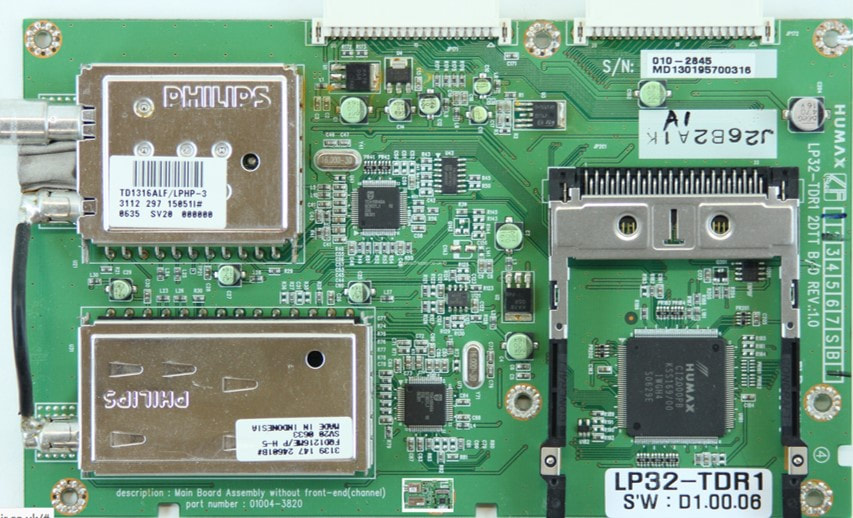

A DVB-T STB reference design around the TDA10046 and PNX8310, including the TD1316L tuner and its TDA6650 MOPLL. [Philips Semiconductors "DTT STB system solution" leaflet, 2003]

Philips Digital Networks also launched a family of Digital Terrestrial Set Top Boxes, the DTR family. This is the DTR1500 from 2002.

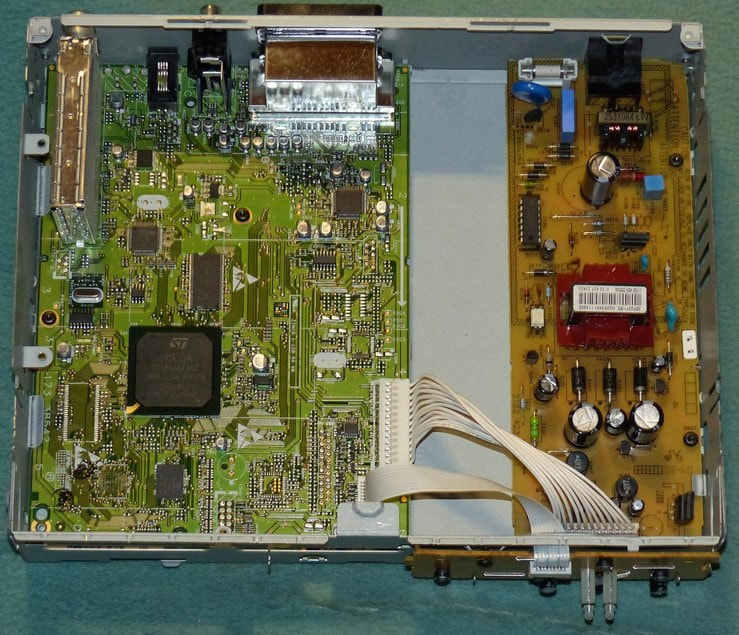

Interior view of the DTR1000, with upper left the TD1316L-Mk1. [Radiomuseum.org]

The TD1316L tuner on the DTR1500 main board. [Peter Vis]

|

The TD1300 appeared in 2002 and was quickly adopted in three application segments:

- PCI DVB-T cards. By this time Semiconductors had developed the new TDA10045 OFDM channel decoder, while the SAA7134 to 46 MPEG decoders and PCI bridge. Especially Semiconductors was a leading player in this domain, promoting many reference designs of these ICs including the TD1300. This was very effective because many customers used exactly this reference design (Hauppage, KNC, Asus).

- DVB-T STB boards. These could also be built using three main building blocks: the TD1300L, the TDA10045/46 channel decoder and the PNX8510-family MPEG2 source decoder. Especially Humax became a leading customer here. Like the VCR in the past also STBs required a loop-through and possibility of re-modulation, and this segment was the driver behind the TDM1300L, with modulator and loop-through.

- TV with DVB-T digital reception as an add-on feature. Philips Consumer Electronics and Semiconductors rather early aligned on the concept of dedicated Intelligent Bolt-on (IBO) cards very similar to STB boards but with interfaces to the BOCMA and Hip-Hop ICs of the main TV and based on PNX852x ICs. The first TV model to use such an IBO-board was the 32DW5658 based on the A10E, the (former) Dreux Mid End CRT chassis. The 2004 LC4 LCD chassis was the first to have DVB-T as an option throughout the chassis.

Block diagram of the TDM1300AL upgrade of the initial TD1300L family. Most options are around the RF in/output, in blue, with between brackets the indicator in the model's name. [Philips TDM1300AL Data Sheet, 2003]

It quickly turned out that two minor but essential updates of the TD1300 concept were required for optimal market acceptance:

- the modulator became an essential and default element of the module, allowing early STB solutions to operate the same way as previously the VCR, so with remodulation of the demodulated and decoded digital TV stream as a standard analogue signal on a UHF carrier. The standard product thus became the TDM1300.

- addition of an input Low Noise Amplifier (LNA) to compensate for the insertion losses of the many splitters and diplexers in front of the tuner. A wideband BFG540W bipolar transistor was used twice, once as input and once as output amplifier.

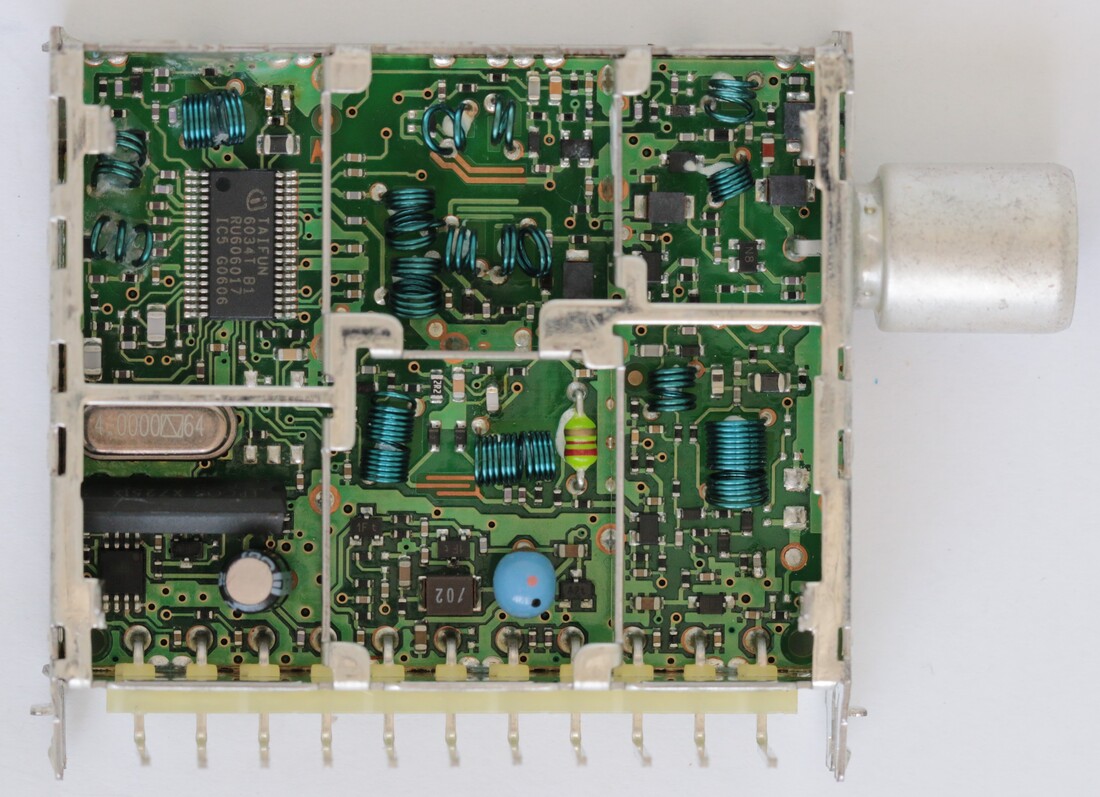

Rare interior view of the TDA1316L/IHP. From upper right clockwise: input section, the UHF modulator, VHF section, DC/DC-converter, SAW filter and IF AGC amplifier, MOPLL, UHF section. [via Edward Ng]

|

A strange animal: the TDM1331L/FHP36. As the name indicates the 31 refers to an NTSC receiver. However, the 36 refers to an IF of 36,15MHz. So, this was a PAL tuner modified for NTSC reception using the standard PAL IF settings.

|

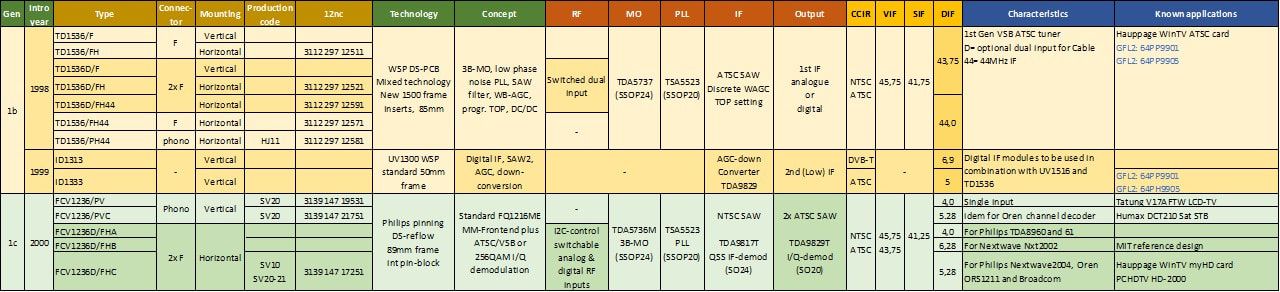

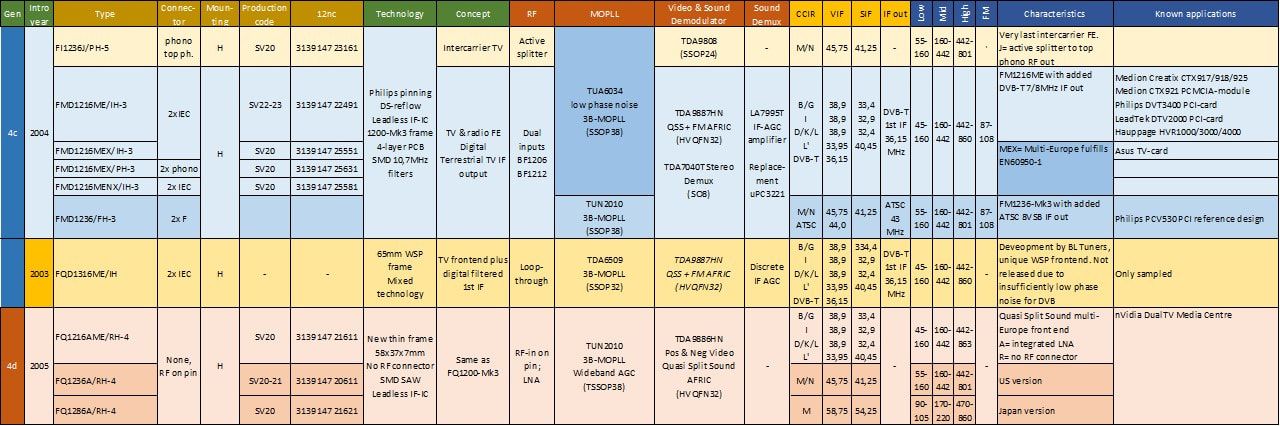

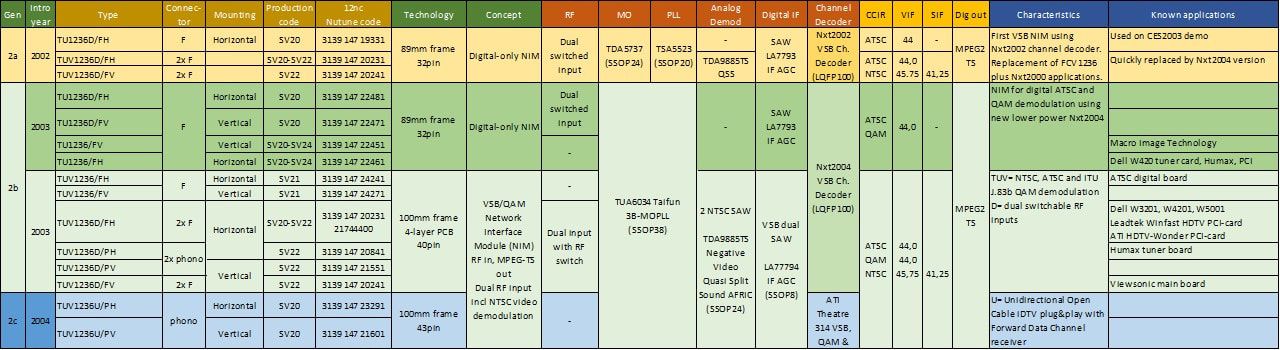

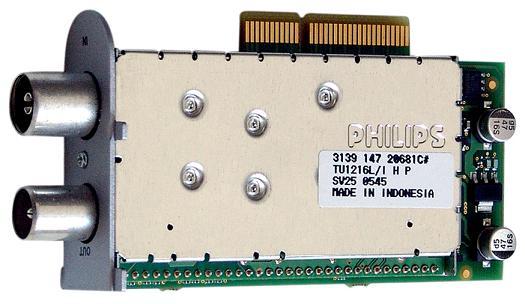

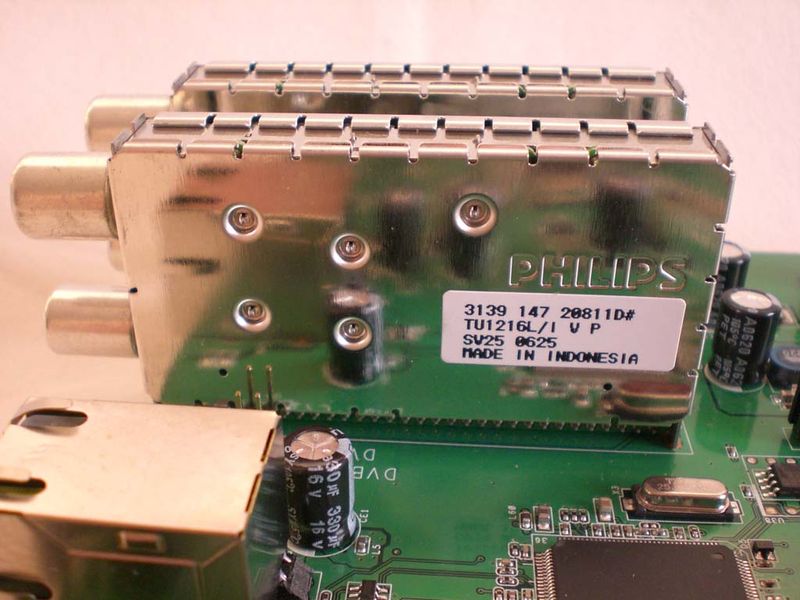

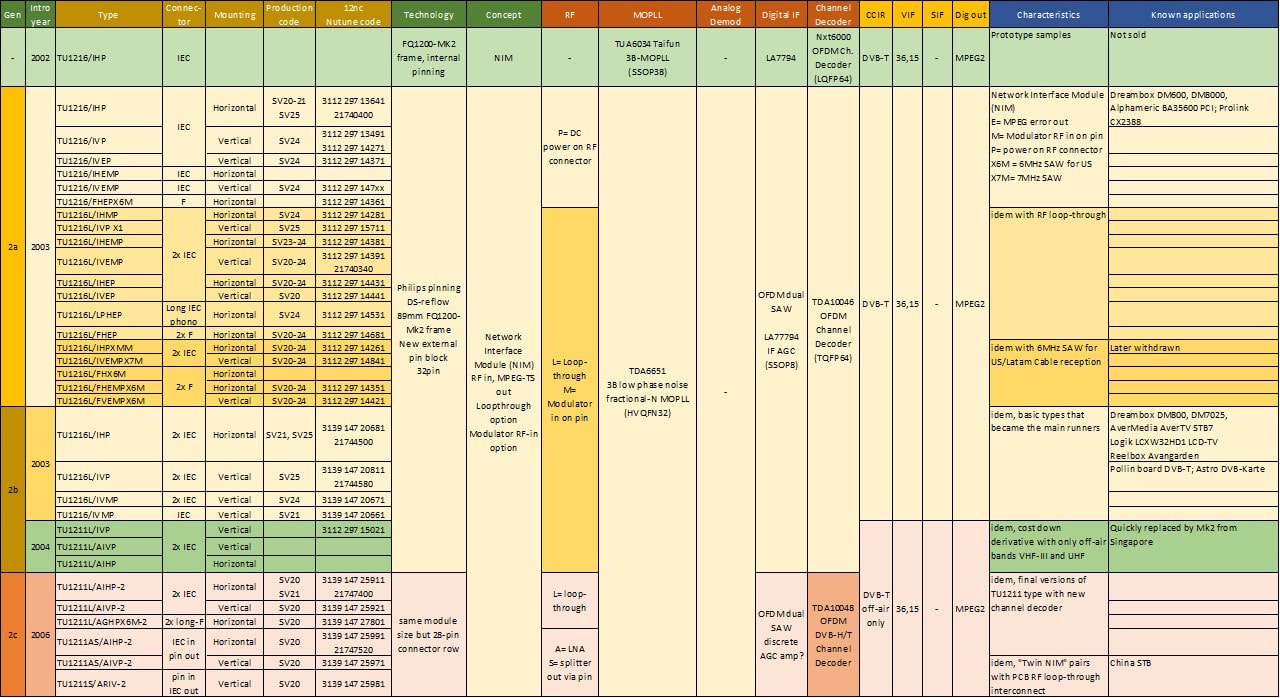

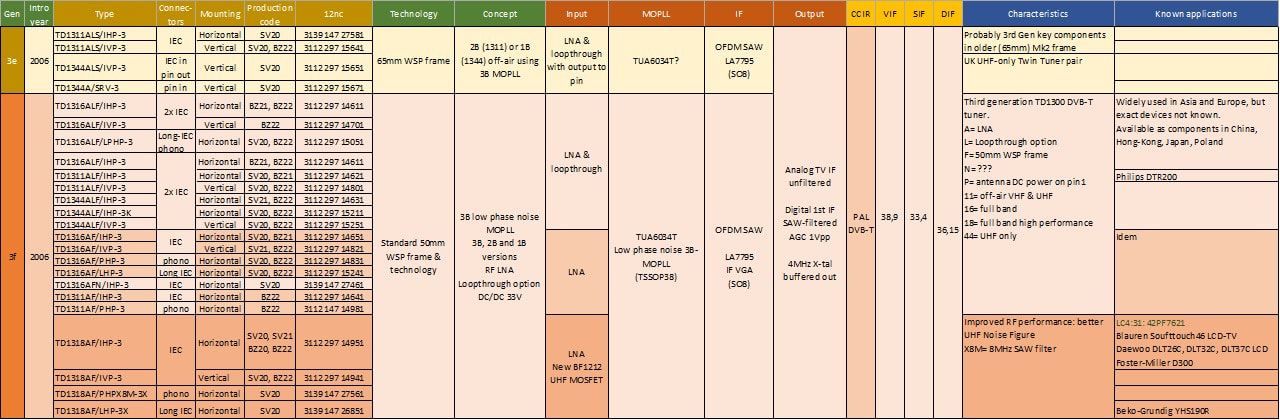

Overview of the first two generations TD1500 and TD1300 Philips DVB-T digital terrestrial OFDM tuners. Although initial production was sometimes Kwidzyn (manufacturing code HJ11 or 21), volume production was always in Singapore/Batam (SV20-24). Some main runners, mainly TDM1316s, were also transferred to Suzhou (BZ22).

Tuner Theory 15: Fractional-N PLL

Fractional-N PLLs were introduced for two reasons:

Standard tuner PLLs like the TSA5521 and 5523 used an internal reference frequency of 7,812kHz, which was obtained by dividing the 4MHz reference crystal frequency by 512. The wanted LO frequency was generated using a divider ratio of 8N in the main loop (so fixed divide-by-8 plus programmable divide-by-N). Therefore, the LO frequency step size was 8 times 7,812=62,5kHz. In case of a different step size a different crystal frequency was required. See the PLL introduction in Chapter 4. The phase noise of the PLL is the phase noise of the (4MHz divided by 512) comparator frequency multiplied by 8N. The phase noise of the LO is thus 20log(8N) dB higher than that of the reference. For the lowest UHF channel 21 (474MHz) we find 8N = 7904 and the phase noise penalty of 78dB.

- better phase noise

- adaptability to different standards

Standard tuner PLLs like the TSA5521 and 5523 used an internal reference frequency of 7,812kHz, which was obtained by dividing the 4MHz reference crystal frequency by 512. The wanted LO frequency was generated using a divider ratio of 8N in the main loop (so fixed divide-by-8 plus programmable divide-by-N). Therefore, the LO frequency step size was 8 times 7,812=62,5kHz. In case of a different step size a different crystal frequency was required. See the PLL introduction in Chapter 4. The phase noise of the PLL is the phase noise of the (4MHz divided by 512) comparator frequency multiplied by 8N. The phase noise of the LO is thus 20log(8N) dB higher than that of the reference. For the lowest UHF channel 21 (474MHz) we find 8N = 7904 and the phase noise penalty of 78dB.

|

Reducing N thus makes a lot of sense for phase noise reduction, critical for OFDM reception. In the TDA6651 PLL two major changes were introduced: the phase detector frequency increased from 7,8kHz to 1, 2 or 4MHz. Secondly N became fractional k/q, with k and q both programmable. Fractional dividing ratios are obtained by ignoring pulses in so-called bit-swallowing counters. The total divider ratio now became (N + k/q) and the total PLL equation Flo = (N + k/q) * fcomp.

|

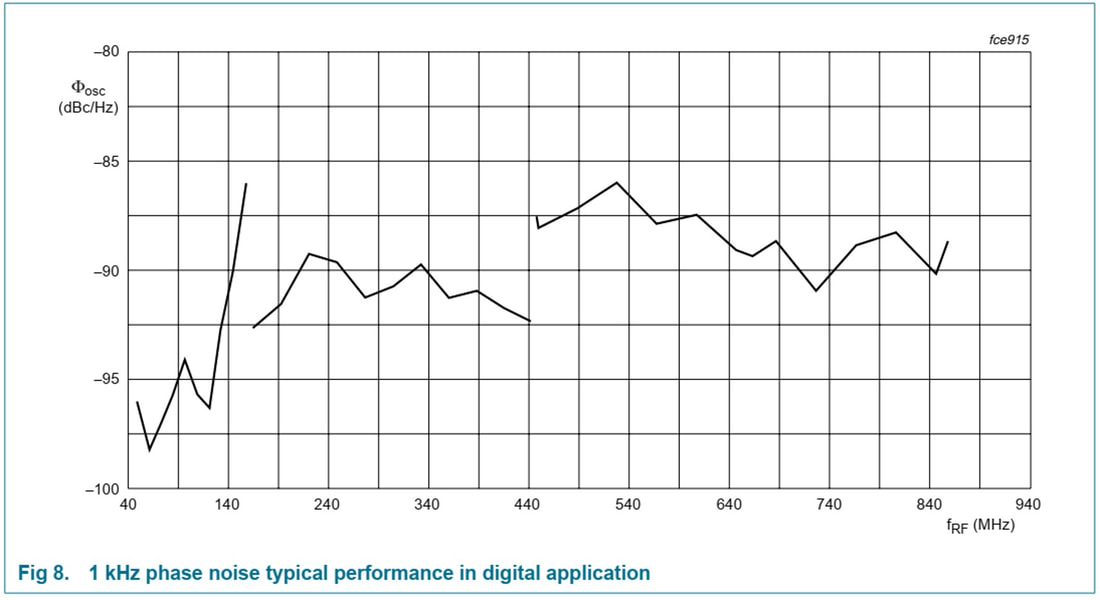

Typical close-in 1kHz phase noise in the different bands of the TDA6651 fractional-N PLL. [Philips Semiconductors TDA6651 Data Sheet]

|

For DVB-T in the UHF band channel width is 8MHz and the channel centre frequencies are given by

474 + (M-21)*8 [MHz] with M the channel number from 21 to 69. The LO frequency is 36,15MHz higher, and thus 510,15 + (M-21)*8 [MHz]. If we take the first channel (M=21) and the highest possible comparator frequency of 4MHz we get:

510,15 = (N + k/q) * 4 [MHz] where N, k and q must be integers. Now 510,15/4= 127,538 = (N + k/q). It can be proven that N=127, k=13 and q=24 is a very good approximation to this solution.

The result of all this is now a step size of fcomp/q = 4MHz/24=166,67kHz, a divider ratio N that is 8 times (18dB) lower than the 8N from the classical PLL. Especially close to the carrier (1kHz) this improvement is manifest, exactly where the phase noise contribution is highest.

Similarly we find for

ISDB-T: 4MHz, k=1, q=28, step size 142,86kHz

ATSC: 1MHz, k=0, q=20, step size 50kHz

474 + (M-21)*8 [MHz] with M the channel number from 21 to 69. The LO frequency is 36,15MHz higher, and thus 510,15 + (M-21)*8 [MHz]. If we take the first channel (M=21) and the highest possible comparator frequency of 4MHz we get:

510,15 = (N + k/q) * 4 [MHz] where N, k and q must be integers. Now 510,15/4= 127,538 = (N + k/q). It can be proven that N=127, k=13 and q=24 is a very good approximation to this solution.

The result of all this is now a step size of fcomp/q = 4MHz/24=166,67kHz, a divider ratio N that is 8 times (18dB) lower than the 8N from the classical PLL. Especially close to the carrier (1kHz) this improvement is manifest, exactly where the phase noise contribution is highest.

Similarly we find for

ISDB-T: 4MHz, k=1, q=28, step size 142,86kHz

ATSC: 1MHz, k=0, q=20, step size 50kHz

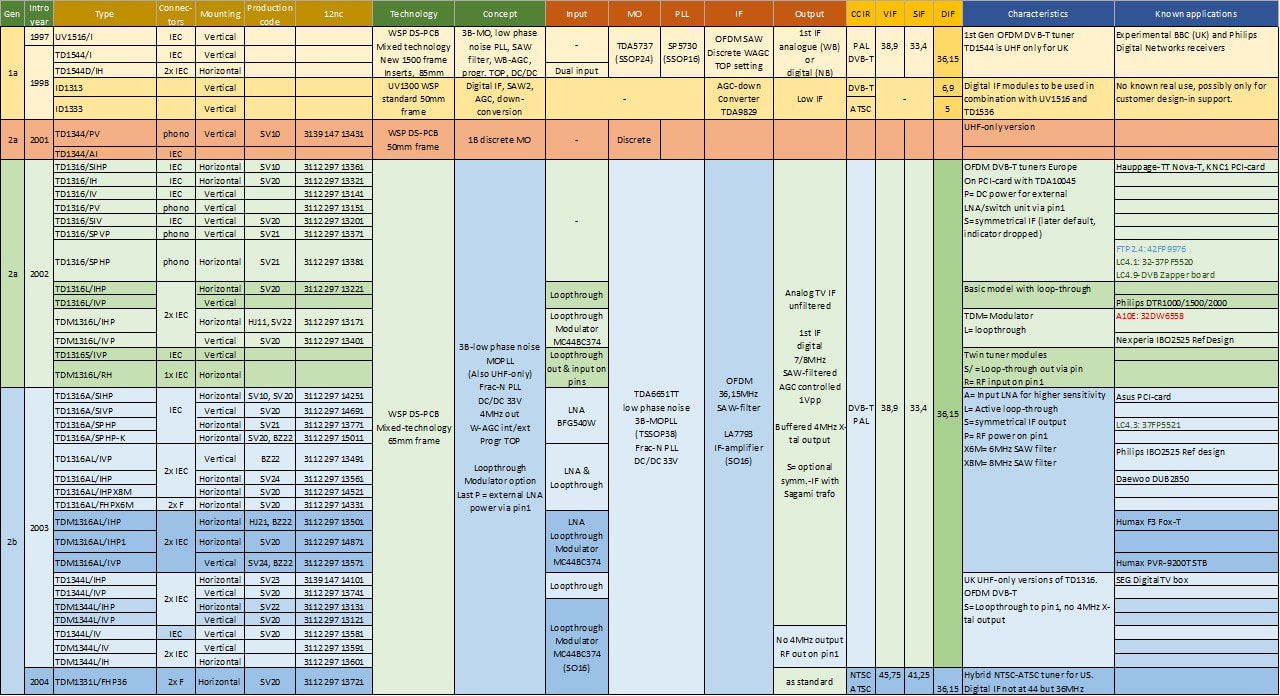

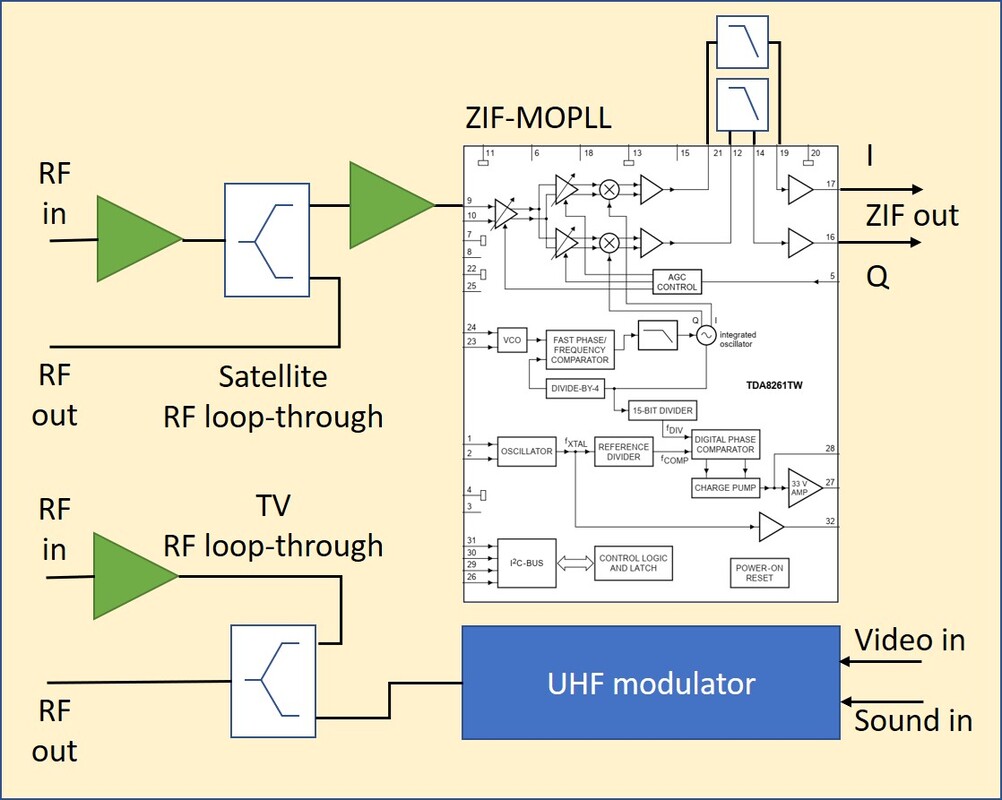

Overview of the different MOPLL ICs used in BU Tuners and BL RF Solutions and Nutune from the year 2002. After the TDA6650 fractional-N PLL Philips stopped developing tuner MOPLLs, nstead focussing on Si Tuners. Infineon, in contrast, brought out a last family of MOPLLs in 2006/7 focussing on higher functional integration.

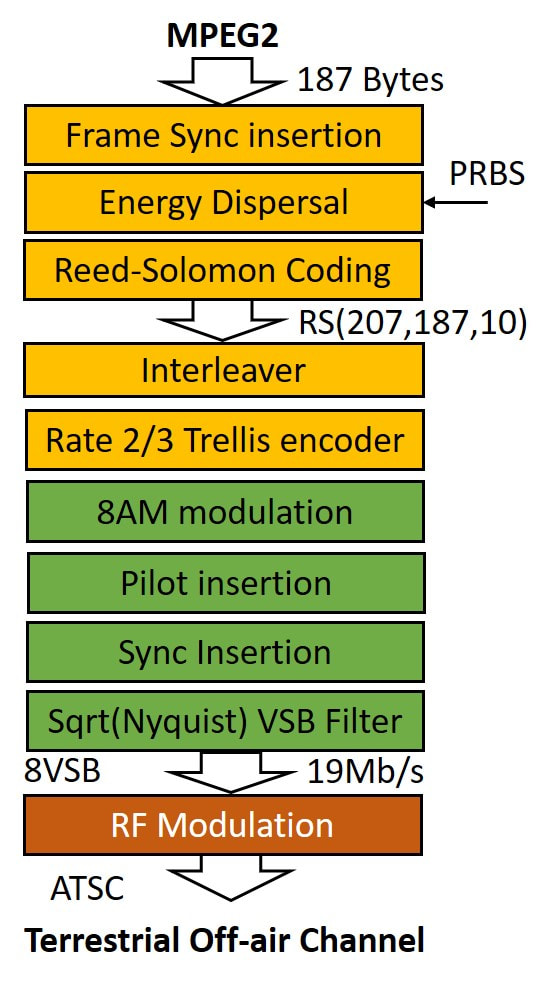

ATSC 8-VSB digital terrestrial TV in the US, 1998

Upstream encoding (yellow) and modulation (green) of ATSC 8-VSB digital TV.

|

Parallel to the dominant European digital TV standardization (DVB-S, DVB-C and DVB-T) the US drove its own standards through the Advanced Television Systems Committee (ATSC) for two main reasons: politically it could not accept the European dominance in the standard setting, while secondly the US broadcasting (NTSC) suffered from the 6MHz channel bandwidth, defined back in 1941 when that was still considered large enough. To come to roughly identical digital transmission capacity per channel required higher order modulation schemes. As already introduced in the DVB-C section the US Cable solution was straightforward: instead of the DVB-C 64-QAM the US standard became 256-QAM, achieving 38,7Mb/s in a 6MHz channel. For all clarity, this was not an ATSC standard, but driven by the ANSI Society of Cable Telecommunications Engineers (SCTE). Because in the US every cable operator is legally allowed to select its proper solution, 256-QAM became the de facto standard.

|

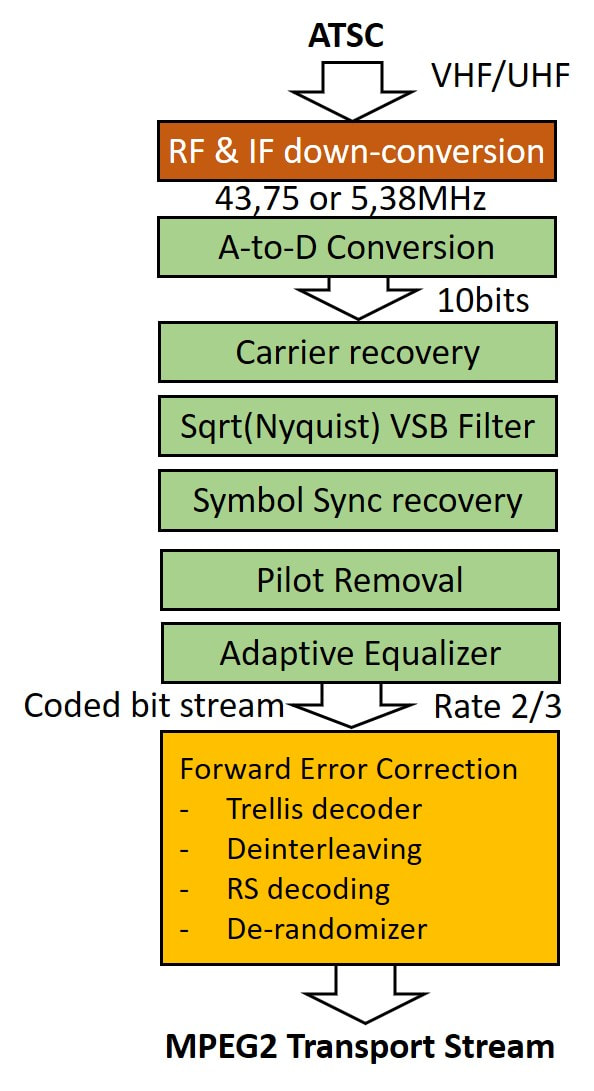

Downstream demodulation and decoding of ATSC 8-VSB digital television.

|

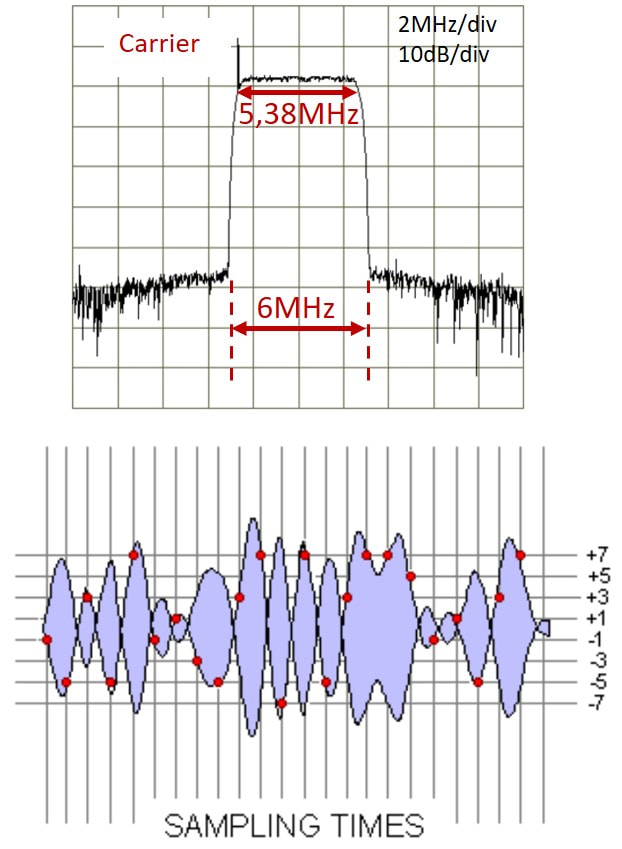

The spectrum of 8-VSB (top) and time domain signal (bottom). Due to the Nyquist filtering the signal is always at one of the 8 levels at the moment of sampling. [Sparano]

|

The ATSC standard started back in 1993, when the FCC triggered the creation of the Grand Alliance, a consortium of the main US electronics and communication players (not necessarily US companies, Philips also participated, next to AT&T, General Instruments, MIT, David Sarnoff Research, RCA-Thomson, and Zenith) to define standards for HDTV and its transmission. However, standards setting in the US is a different process than in e.g., Europe or Japan, where it is mostly left to the technical community to come with consensus on the "optimal" technical solution, which is then possibly twisted by politics when the French or British have their usual objections. The Grand Alliance, in contrast, was not a consensus-driven exercise, but the big players simply divided the tasks amongst them based on eagerness, claims or lack of others interested. Since Philips was mainly interested in harmonizing the HDTV formats, the transmission standard was left to Zenith, the last remaining US TV maker, which promoted its 8-VSB concept. (A similar single company driven standardization would happen a few years later with the Qualcomm CDMA standard for 3G telecom). It was accepted and published by the FCC as standard A/53 in 1996. Interestingly, in 1995 Zenith, nearly bankrupt, was acquired by Korean Lucky Goldstar Electronics (LG), so in the overviews of 8-VSB patent owners you will find this company at the top of the list.

The 8-VSB modulation is most similar - but also very different - to QAM, so we'll compare it with that standard. The encoding part of ATSC A/53 is fortunately very similar to DVB-C, with a slightly different Reed-Solomon. A Trellis-coder translates 2 bytes into one 3-bit byte, which is used for 8-level Amplitude Shift Keying (8-ASK). For ease of clock recovery, a pilot is inserted by creating a DC offset, followed by Segment (208 bytes) and Field (313 Segments) sync bytes insertion. |

|

At this point the signal is a 10,76MSymbols/s classical 8-ASK double side band signal with pilot carrier and several rapidly diminishing side lobes. This signal is now applied to a rigorous square-root Nyquist filter, eliminating all signal left of the carrier, and reducing the signal bandwidth to just half the symbol rate: 5,38MHz. With a roll-off relaxation of 11% this is equal to the 6MHz NTSC channel width.

Although this method allows to squeeze 19Mbit/s into a 6MHz radio channel, the effect of the Vestigial Side Band (VSB) asymmetric filtering on the signal waveform is serious: major phase and amplitude distortions happen due to ringing of the individual symbol filter responses. There is only one escape for proper detection: when clocked with the symbol rate frequency all these filter responses are orthogonal - like in OFDM - meaning that they are all equal to zero at all sample moments other than their own. This results in a small yet open eye pattern, so far assuming no multi-path fading. At the same time the peak-to-average ratio of the signal is high, requiring a roughly 10dB back-off in the transmitter and receiver to avoid non-linear distortion.

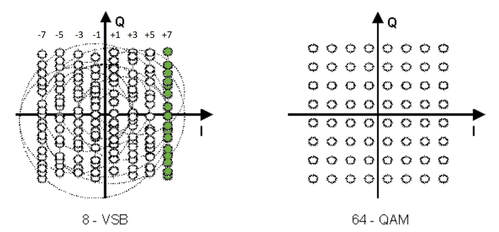

An 8-VSB constellation diagram (left) and 64-QAM (right). Where QAM uses both the I and Q axis for encoding, 8-VSB only uses the real axis for amplitude modulation. However, due to the VSB filtering phase distortion can move the constellation points along the Q axis. In the example all green constellation points should be detected as +7 (111). [All 8-VSB illustrations in this section are from Sparano "What exactly is 8-VSB anyway?", a very useful introduction to the standard.]

|

Two views at the received time domain 8-VSB signal. The top graph shows an instantaneous trace (black) and a time-averaged trace (purple). Below the eye pattern. [Sparano]

|

From the moment the Grand Alliance, ATSC and FCC (in that order) standardized 8-VSB a heated debate emerged: why choose an unsophisticated VSB scheme when the rest of the world was convinced OFDM was by far the best solution for dealing with multi-path fading? The FCC maintained VSB to be more robust to fading, while also better in so-called fringe areas with low received power. The latter is true if 9m high antennas are used, a solution more common and acceptable in the US than in Europe and Japan, where large external aerials are often forbidden. To compare 8-VSB to OFDM on multi-path robustness tests were done, although allegedly using non-optimal OFDM receivers. It is a fact, though, that the first VSB demodulator ICs like the Philips Semiconductors TDA8960, could only compensate echoes between -2 and +10ms, whereas DVB-T OFDM allowed -100 to +100ms when using the maximum guard interval. Only after 5 to 6 generations of VSB decoders the echo equalizer performance came at roughly half that of OFDM. But whatever the technical outcome would have been, the FCC never intended to adopt OFDM simply because they wanted their own standard, even at lower performance.

|

It should not be forgotten that ATSC A/53 specified both a terrestrial system - using 8-VSB - and a cable system - using 16-VSB given the better SNR on cable networks - but the latter was largely ignored by the cable operators, deploying 256-QAM instead. VSB would thus be limited to off-air reception in the US, Canada, and a few Caribbean and Pacific islands. Because of all discussions about the technical merits of 8-VSB, deployment started very slowly, despite a lot of political pressure, first transmissions taking place in 1998. Obviously, Philips, as member of the Grand Alliance, was eager to participate, both with modules (BL Tuners!), ICs (Semiconductors), Set Top Boxes (Digital Networks) and TV sets (CE-BGTV). To this end a dedicated development lab was created in Briarcliff (New York) near the US Philips Research Lab there. In 1998 and 1999 Philips was one of the first brands to release ATSC-ready sets. These were super high end HDTV 64" rear projection sets from Brugge, the 64PP9901 and 64PH9905, both almost certainly based on the GFL2 chassis.

The outcome of all these developments was that also for digital TV the US continued to require its dedicated tuners. |

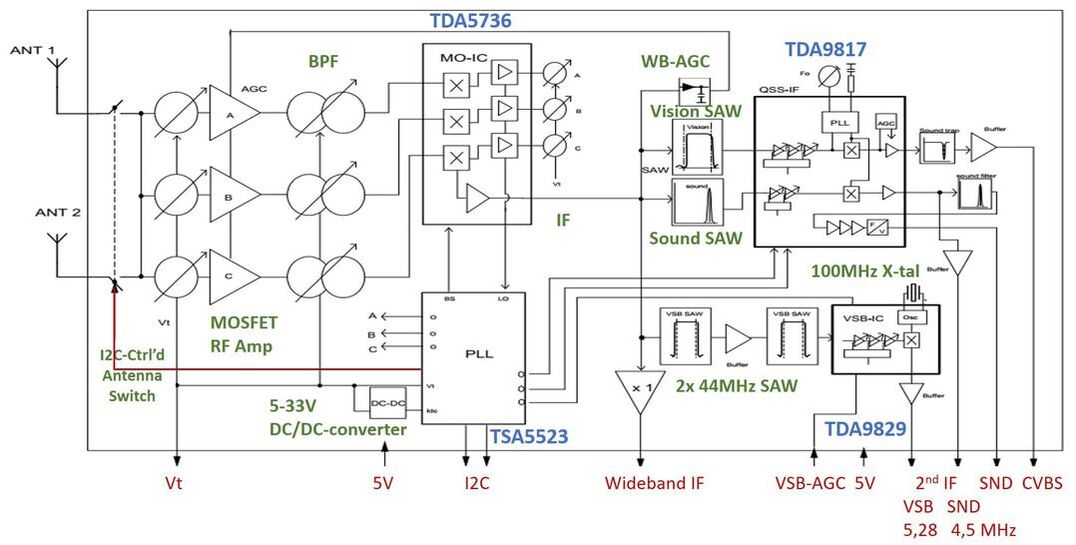

TD1536 and FCV1236, the first ATSC support, 2000

As member of the Grand Alliance and eager to be a leading player in the worldwide HDTV roll-out, the company pushed hard to get a first ATSC-ready set out by the time the standard was released, and experimental transmissions started. The BU Tuners, like the OFDM developments taking place in parallel, used the 1500-platform for these emerging digital standards. For ATSC this was the TD1536, conceptually identical to the TD1516 for OFDM but with the IF at 43,75MHz or 44MHz in line with the standard NTSC intermediate frequencies (45,75MHz Picture Carrier and 41,25MHz Sound Carrier). The TD1536 was used in the 64" rear projection TVs introduced above, developed in Brugge based on the GFL2 chassis. The NTSC receiver used the standard FQ936-(Mk2) analogue front end. It likely used a PS1311 RF splitter, and - so far not formally confirmed - was possibly the only time the ID1333 second IF module was actually used in a product.

The Philips TD1536D/F, dual input ATSC tuner. Lower right the DC/DC-converter, in the leftmost section the IF SAW filter and amplifier. [via Darko Jancin]

|

Still based on the proven TDA5737 MO and TSA5523 PLL the tuner offered high performance with respect to phase noise and tilt. The DC/DC-converter for supplying the 33V varicap bias, copied from the FQ1200 multimedia frontends, was an important feature for PCI applications. The dual inputs allowed the tuner to be connected to both an off-air antenna as well as the local cable distribution, also because it could handle both 8-VSB and 256-QAM modulation.

|

Although the super high-end TVs were publicity-wise a good show, initial volumes were not in TVs with ATSC boards. Especially in the US the PC market was much more eager to start experimenting with the new technology, and PCI-cards thus required ATSC tuners. Philips Semiconductors and the BU tuners jointly brought out the "Coney" Reference Design, based on the latest solutions shown in the block diagram. The first to apply this architecture in a product was Hauppage, with its WinTV PCI-card. As in the first TVs this was a high performance solution, unsurpassed by any competition, but with one major drawback: the size of the module. A functional shrink was urgently required.

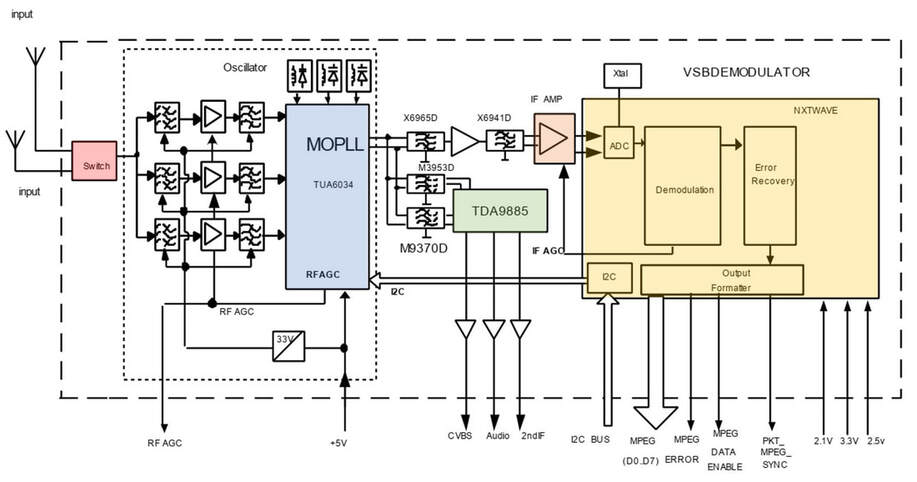

Block diagram of the Philips Semiconductors "Coney"ATSC reference design for PC applications. The TD1536 tuner and TDA8960 8-VSB channel decoder were the ATSC-specific new components. [Philips Semiconductors Coney leaflet, November 1998]

|

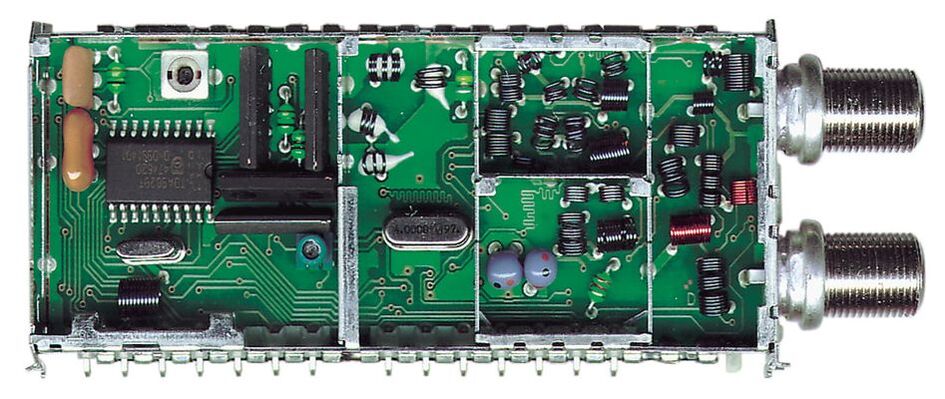

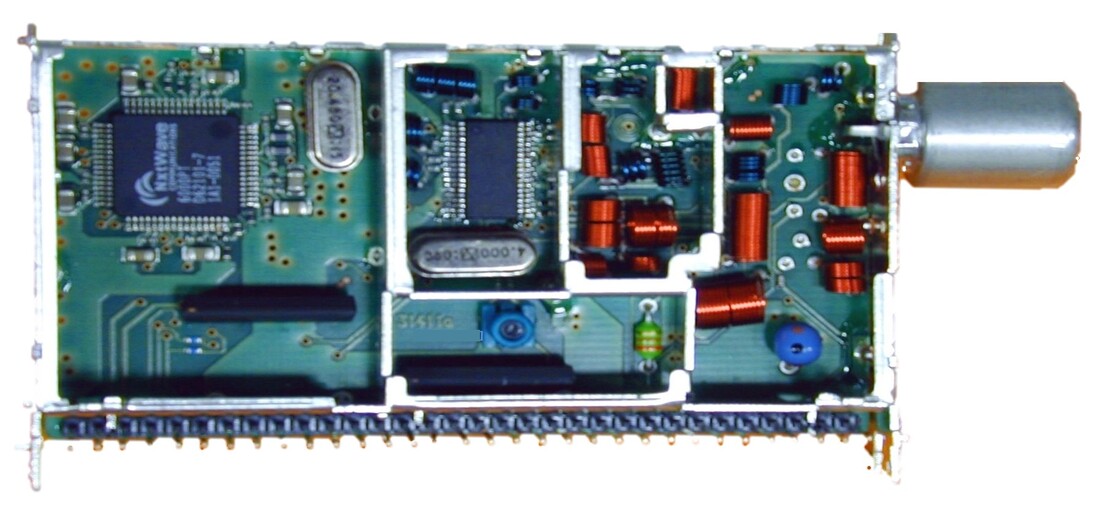

Hauppage WinTV ATSC/NTSC PCI-card, the first to implement the Coney reference design including the TD1536D/F. Note the still very low level of integration, resulting in many different ICs on the board.

|

Block diagram of the FCV1236D. Note the switchable input and the dual 44MHz VSB SAW filters. [FCV1236D PRS document, via Toh Kong Lim]

Interior view of the FCV1236D/FH. The IF section has the TDA9829 VSB down converter on the B-side, as well as the four SAW filters and two orange sound filters. The high isolation RF switch therefore had to be crammed between the standard tuner and the two connectors. [via Darko Jancin]

|

Because at this point the PC application was driving developments, the need for backward compatibility with analogue-only reception was determined by this domain. Which obviously was the FQ1216-Mk2 family of Multimedia Front ends. The most recent product was the FQ1216ME-(Mk2) using the Quasi Split Sound (QSS) IF demodulator IC TDA9818 for positive and negative video modulation. No QSS NTSC version had been developed yet but using the tuner section of the FM1236 and the negative modulation-only TDA9817 the analogue core of a combo NTSC-ATSC front end was available. To this was added the IF path originally contained in the TD1536 and ID1333: two 44MHz VSB SAW filters with buffers followed by the TDA9829 second down-converter. Three versions were foreseen:

|

|

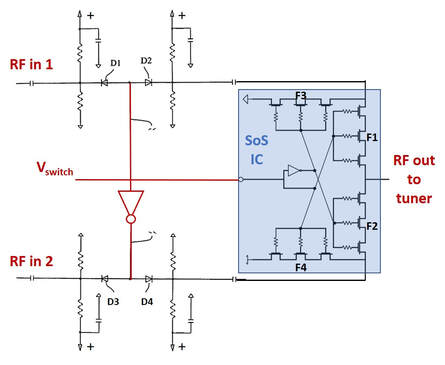

The biggest challenge of the FCV1236 was the dual input, and especially the extreme input-to-input isolation mandated by the FCC of 80dB up to 216MHz and 55dB from there to 801MHz. This was an extremely demanding requirement, especially in the crammed space left for the switch within the 1200 frame. The "standard" solution with common anode diodes did not provide sufficient isolation, so in the end a second RF switch had to be added. This was made in the at the time quite revolutionary new Silicon-on-Sapphire (SoS) technology developed by Peregrine Semiconductors. Due to the sapphire substrate, ground- and substrate parasitics were effectively eliminated. Although the IC initially cost 1,50USD this was deemed acceptable given the healthy margins on these products. All in all, it was a serious struggle to meet the specs, although it did provide a patent.

The FCV1236 started sampling to the different channel decoder players (Oren (from Israel) Broadcom, NextWave (a spin off from Sarnoff Labs) in 2001, but it took till 2003-4 before volumes became interesting, mainly due to a joint demonstrator with NextWave at the 2003 Consumer Electronics Show (CES) in Las Vegas. It was all simply too new, there was limited content, and the supply base was unstable: NextWave was acquired by ATI in 2002, Oren in 2004 by Zoran. In 2003, following the closing of Philips Sunnyvale, also Philips Semiconductors stopped ATSC channel decoder development. Some of these decisions were amplified by the fact that ATSC take-off was very slow until 2005, making it an expensive field to play, with high requirements and investments but minimal sales. |

Circuit diagram of the I2C-controlled RF input switch for the FCV1236. In case Vswitch is high D3 and D4 are in reverse, drawing no current and blocking input 2. D1 and D2 are open, providing a low-Ohmic RF path to the Peregrine Silicon-on-Sapphire (SoS) IC. Here series FETs F1 is open, providing the path to the output. F4 is also open to short circuit input 2 to ground, while F2 and F3 are closed and provide high-ohmic resistances. For Vswitch = low the opposite situation applies.

|

The first two generations of Philips tuner-frontends for 8-VSB ATSC: the TD1536 and FCV1236.

Satellite Developments, 2000-2005

|

By the turn of the century the satellite broadcast market was rapidly stabilizing. Within a very short time all main operators had switched from the analogue FM to digital QPSK transmission, mostly DVB-S or DSS in the US, the main reason being the much higher number of channels that could be transmitted over the same transponder. However, the absolute share of satellite in the TV distribution market was not increasing, remaining at around 25%. Growth came only from the total TV market growth of some 3-4% per year. The 2000 volume was around 23Mio boxes (8 Mio Europe, 12Mio US and 3Mio Asia-Pacific), growing to some 36Mio by 2005.

On the satellite operator side consolidation was taking place. In Europe SES with its Astra satellites became the dominant player, with Sky (UK and Ireland), Premiere in Germany (using Eutelsat) and Türksat (Turkey) as smaller players. In the US DirecTV became dominant. The Astra2 series of satellites now typically transmitted over 32 transponders of 28MHz channel width. |

Astra 2D satellite, based on the Hughes601 spin-stabilized platform. It was launched June 16 2001 on top of a Proton rocket from Baikonour in Kazachstan.

|

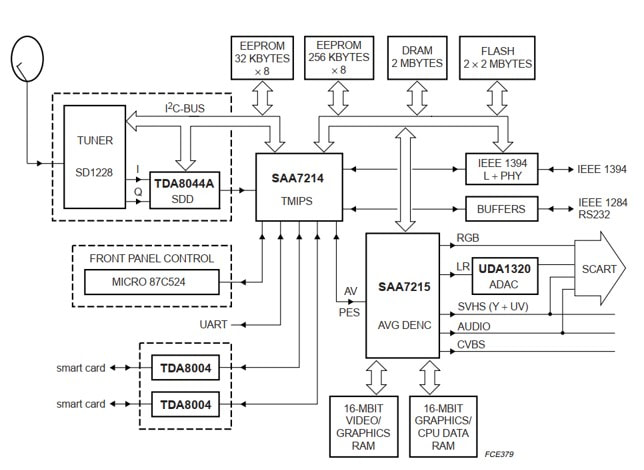

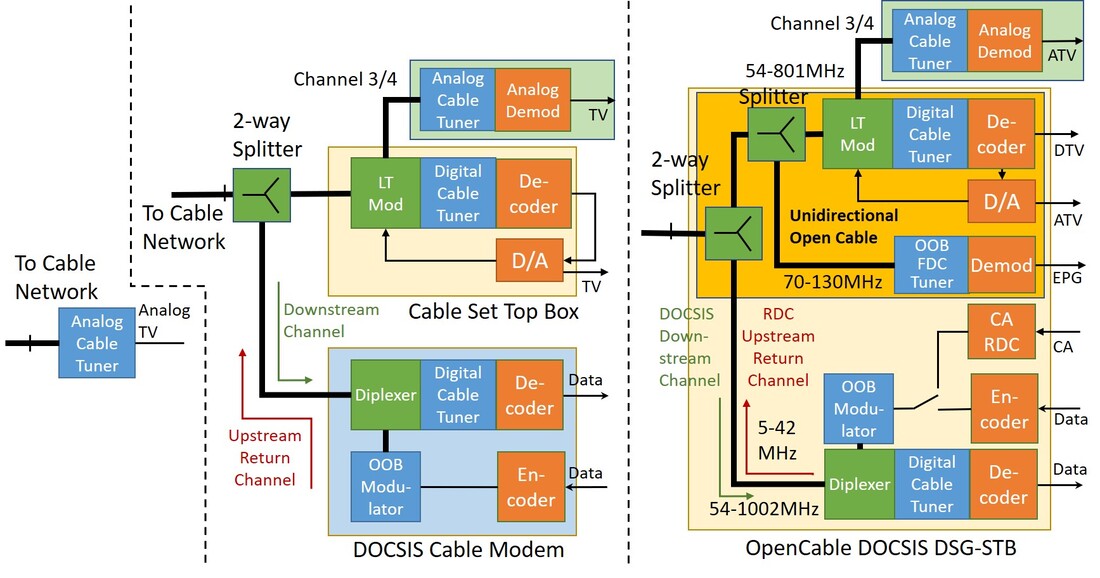

Block diagram of the Philips Semiconductors STB5860 Satellite Set Top Box Reference Design. The SAA7214 is the MPEG decoder, demultiplexer and Conditional Access controller. Except for IEEE1394 all interfaces are still analogue (SCART) provided by the SAA7125. [Philips Semiconductors OM5730 Data Sheet, 1999]

On the device side the Philips business selling Set Top Boxes was Digital Networks (DN), still driven by Rob van Oostenbrugge. This business , with its main development centres in Eindhoven, Suresnes (France) and Sunnyvale (CA, USA) and internal production in Hasselt (Belgium), had grown to 1Bio€ sales in 1999, with outlook on 1,5Bio€. It had obtained, at a 12% market share, the number 2 world-wide position in Set Top Boxes, behind General Instruments (which dominated the US Cable market, 18%) and before RCA/Thomson(which dominated the US Satellite market, 11%). DN was the leader in Europe, especially in Satellite through its main customer Astra, but was growing its business with Echostar and DirecTV in the US. Despite all this, business in STB was tough, for the reason mentioned above: a (low end) STB essentially reduced to the front end function including the channel decoder, a single MPEG demux/encoder and a power supply. Furthermore, all customers demanded their dedicated Conditional Access solution (CA, the smart card with subscription key). Consequently, Philips increasingly used ODM boxes from low end STB makers like Pace (UK), while under pressure of cost reduction they drifted away from Philips Semiconductors to ST Microelectronics, which was becoming the market leader in STB functional integration and the main supplier to market leader RCA/Thomson. Both these trends worked out negatively for the BU Tuners, which saw itself replaced by Alps in more and more platforms.

Four generations of Philips Digital Networks Satellite Set Top Boxes. From the top:

(1) DSX6073 Gold Box (2001) 27,5MS/s, produced Hasselt;

(2) DSR2015 for Premiere (2003), probably a Pace ODM box, introduced DiSecq1 LNB control;

(3) DSR2210 (2004) for Dutch Kanaal Digitaal;

(4) DSR5005 (2006) for DVB-S2 MPEG4 HDTV.

[Sat-Receiver-World.de]

|

Throughout the previous chapters it has been made evident how especially the developments in (silicon) semiconductor technology have been driving product architecture and concepts. Although on the one hand this allowed continuous size and price reduction, the integration also steadily simplified the integral RF design. Many previously complex functions requiring solid RF design knowledge, like oscillators, filters and mixers became integrated and part of the ICs, making the application design around them much easier. The domain where this happened first and foremost was satellite reception. Because of the well-defined and stable transmission path from satellite to receiver, with modest dynamic range requirements, minimal interferers and linearity requirements, satellite reception was the easiest domain to push for total integration.

However, this integration trend not only happened on the front end side of the system, but the digital back end was also integrating at an even higher speed, pushed by the 2,5 year cycle of CMOS node migration. By the turn of the century the standard CMOS node within Philips Semiconductors had become 180nm, with 120nm a weak node that was rarely used. In the partnership with ST Microelectronics in Grenoble (France) 90nm was being developed and rolled out, marking the transition from 200mm (8") to 300mm (12") wafers. This provided a path for continuous integration of all digital functionality, and Philips Semiconductors was an active player in all this.

A major business success of Philips DN, the DSX6000 "Gold Box" family of Satellite STB from 2000. Upper left the SD1228/L-Mk3 front end with loop-through function. [GbC-Net forum]

So in the end both Digital Networks (from the top) and BU Tuners (from the bottom) were squeezed between the reducing sales prices of Set Top Boxes and the growing semiconductor content, leaving hardly any margin for the module maker and set integrator. And this in a domain where developments went extremely fast, with new - even more integrated - chip sets every year, demanding a substantial development effort. Not to forget the growing number of services, copy protection (Philips used Macrovision), new concepts like Astra Multimedia Home Platform (MHP), DiSEqC LNB control and towards 2005 the new standard DVB-S2, based on MPEG4 H.264 HDTV video encoding and using 8PSK (or higher) modulation.

In 2002 DN was hit by the same re-organisation that dissolved the PD Components, which meant that all US STB activities from Sunnyvale were discontinued. In Europe manufacturing in Hasselt was closed and transferred to Szekesfehervar in Hungary. In 2004 DN was dissolved as a Business Group and the remains of the STB business integrated into the new BG Home Entertainment Networking under Consumer Electronics. The BU Tuners/RF Solutions did not fare much better, and after a last effort with Network Interface Modules, also had to throw in the towel in the domain of satellite. |

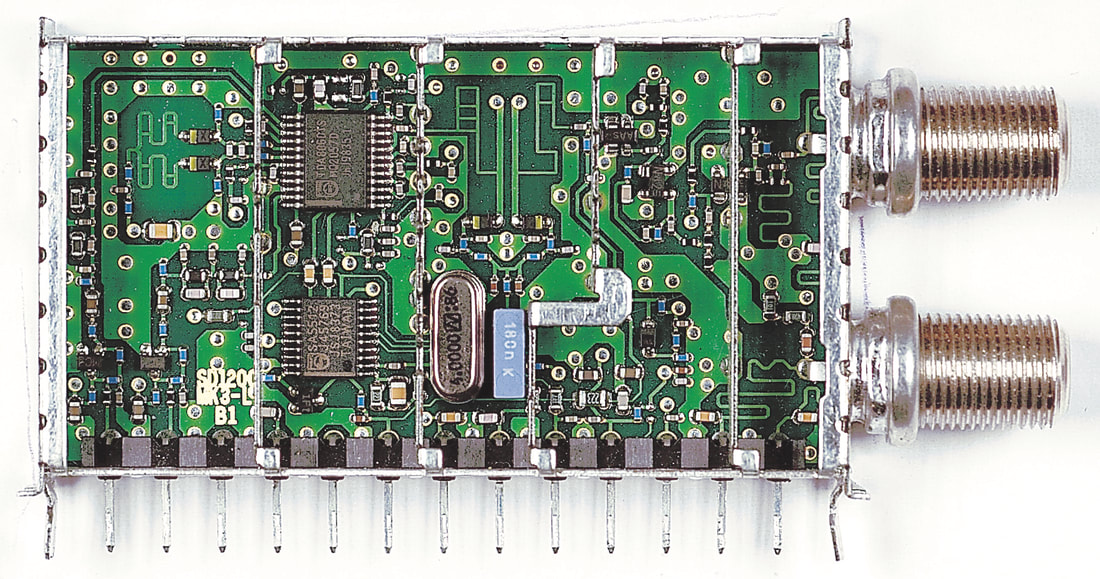

SD1200-Mk3, 2000

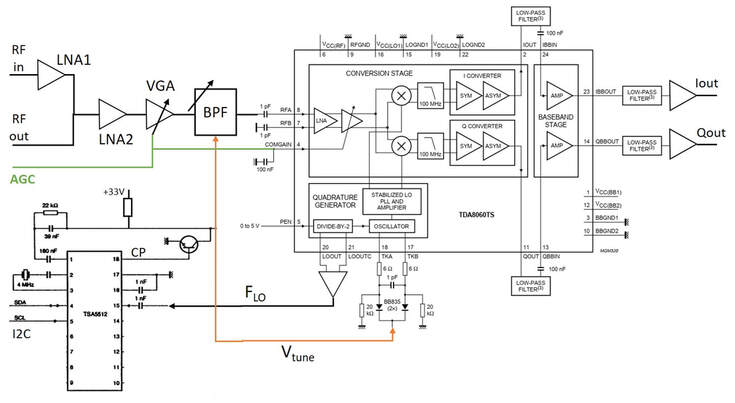

Although the year before, 1998, the SD1200-Mk2 family was released, developments in integration went so fast that already the year after the Mk3 generation had to follow. Where the Mk2 had made major integration steps with the TDA8010 mixer-oscillator and TDA8024 IQ IF demodulator, the introduction of the TDA8060 Zero-IF (ZIF) MO made both these ICs immediately obsolete. With the ZIF architecture Intermediate Frequencies are reduced to DC, and the MO output can, after proper low pass filtering and amplification, be fed directly to the ADC inputs of the channel decoder. Furthermore, with the ZIF architecture tracking was reduced to having the input BPF and the LO tank circuit centred at the same frequency, much easier than tracking at 480MHz distance. Even the application of the TSA5512 PLL was reduced to its core function since any switching or AFC could be omitted.

Block diagram of the SD1200/L-Mk3. The RF function has reduced to a few amplifier stages and the tunable BPF. The AGC control signal comes from the channel decoder.

Tuner Theory 16: Zero-IF receivers

From the first TV tuner in 1951 till the year 2000 all tuners and receivers that have been presented were based on the heterodyning principle: the Local Oscillator (LO) frequency is off-set (usually above) the incoming RF signal, producing, when mixed in a non-linear device, the difference Intermediate Frequency (IF). One of the main difficulties of tuner design over all these years was the required frequency-dependent filtering: RF Bandpass Filters (BPF) before the mixer and fixed SAW filters in the IF. The challenge was good filter performance across substantially large tuning ranges. Not only did this require a lot of detailed RF design knowledge, the cornerstone of the Tuner business, more importantly these filters are impossible to be integrated in silicon devices. This is mainly due to the high RF signal path losses on silicon, caused by the lossy substrate, which limits the attainable Quality factor of inductors, which in turn means (RF BPF) filters on silicon show high insertion loss. Finally, when trying to increase the filter Q, the inductors tend to become relatively big, making them expensive in advanced silicon technology. It was therefore obvious that, to push receiver integration, the classical heterodyne architecture had to be replaced by one that supported (almost) full integration.

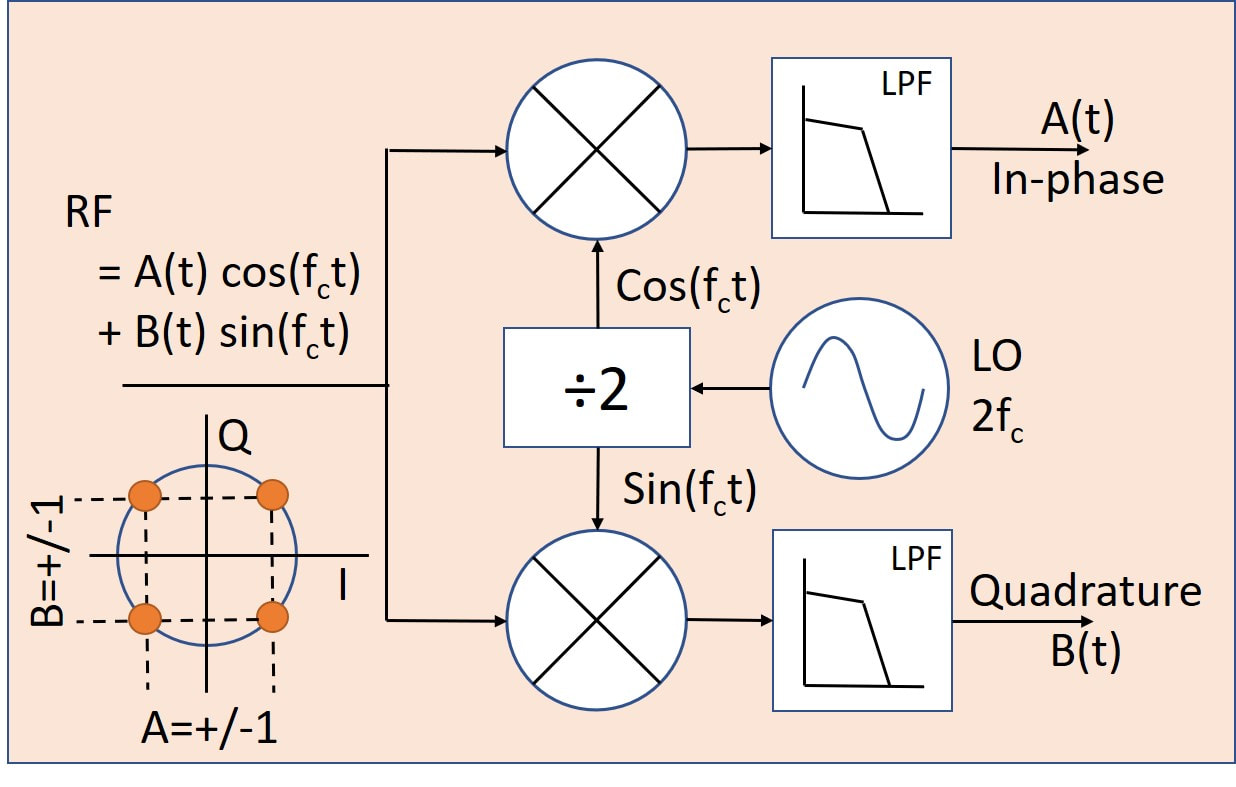

The solution to this is the so-called Zero-IF (ZIF) concept, although it is equivalent to the more classical terminology "coherent receiver" or "synchronous detector". In all cases the concept is the same: the incoming RF signal is mixed with an LO of the same frequency, thus resulting in an IF equal to zero Hertz. When the RF signal was modulated, the modulation will now be around DC in baseband. Furthermore, when this is done with two coherent orthogonal In-phase (cosine) and Quadrature (sine) components of the LO, the two outputs effectively deliver the I and Q (or real and imaginary) modulation components. See the figure below.

The Zero-IF concept.

From the above diagram the advantages are evident: no (tunable) BPF anymore, only easy to integrate LPF and the sine and cosine LO components are easily generated in a divide-by-2 circuit. A few remarks, though: for proper matching the RF input still requires some broadband matching filter; the Noise Figure of the mixers is very bad, requiring an (external) LNA; proper I-Q phase alignment is very critical and might need active control; the LO usually still requires an external tuned tank circuit. Also, the LO phase noise requirements are higher!

ZIF was first implemented in Philips DECT cordless phones, followed by the narrow band 2G and 2,5G GSM receivers. Satellite was the first wideband application using ZIF. |

There was now more than enough space on the B-side for all SMD components, while the number of manually placed components reduced to two: the X-tal and a charge pump capacitor. The wave soldered A-side was essentially empty and only used for DC distribution and grounding.

B-side interior view of the Philips SD1228/L-Mk3 satellite frontend. The upper F-connector is the input, the lower one the loop-through output. The second section contains the LNAs, the third one the tunable planar BPF (note the two varicaps at the foot of the filter), the fourth section the ZIF-MO and PLL, and the leftmost section the symmetrical LO tank circuit (again with 2 varicaps) and the output LPFs (discrete) and amplifiers. [via Darko Jancin]

In parallel to the SD1200-Mk3 for digital satellite, a very last analogue FM satellite front end was released, the SF1218D-Mk3, using the same ZIF architecture and chip set. In fact, with the ZIF architecture analogue and digital receivers had become identical, apart from minor details like the bandwidth used.

Another special version was the SD1278-Mk3, like its Mk2 predecessor specifically for bitrates as low as 1MS/s. This required the TSA5059 low phase noise PLL, which allowed much higher comparison frequencies to reduce the divider multiplied phase noise. With five I2C-controled bits the phase comparator frequency, and thus the PLL step size, could be selected between 12,5kHz and 2MHz. This PLL would also become the standard PLL in the next generation.

The SD1228/LH-Mk3 in the Philips DSX6073 Gold Box Satellite STB introduced 2001. Note that the box is becoming very empty. The largerst IC on the board is the ST Omega MPEG decoder. [Radiomuseum.org]

The SD1200-Mk3 family was still reasonably successful, being used in all DSX5000 to DSX7000 Philips DN Set Top Boxes. However, both were suffering from severe added-value reduction, and thus margin pressure. From 2000 to 2002 the satellite sales of the BL reduced by a factor two; something needed to be done.

|

Overview of the Philips SF/SD1200-Mk3 satellite front ends family. The production code HJ indicates they were all produced in Kwidzyn, Poland. This family was mainly used in the Philips Digital Networks satellite STB range.

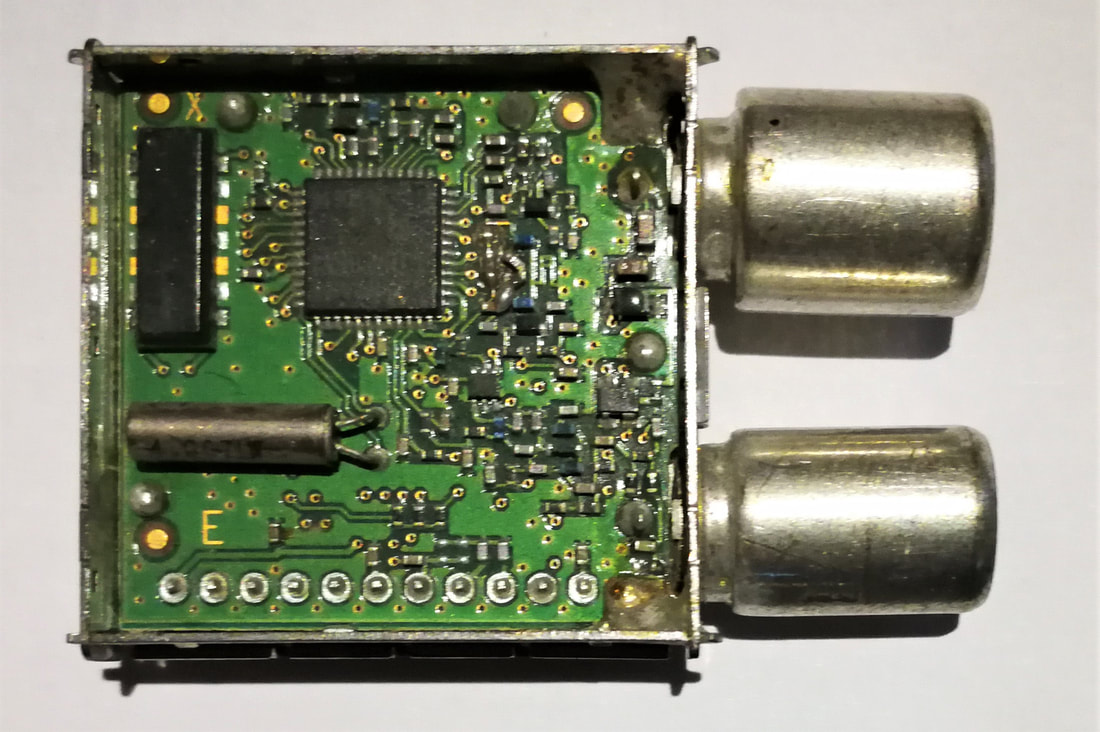

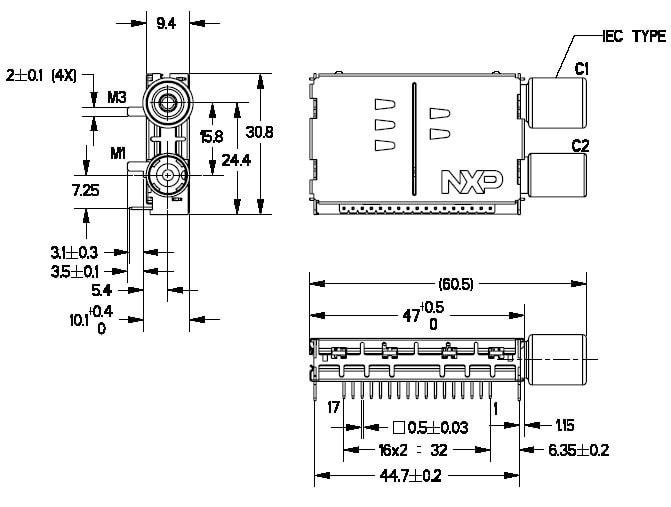

SU1278, the first NIM, 2001

Satellite RF and IF functional integration was thus happening very fast, at this stage (around 2000) reducing the satellite front end to just two ICs (a ZIF MO and a PLL) with limited RF application around it. And coming soon was the next integration step, the ZIF MOPLL on which Philips Semiconductors (the TDA8260), Infineon (TUA6100) and ST Microelectronics were all working. With both sales price and margin reducing, some form of functional integration was needed to add value back to the module. The answer was the Network Interface Module (NIM), the integration of the RF and channel decoder functionality into one module, thus delivering a very convenient RF-to-MPEG Transport Stream converter. The NIM had several advantages:

- Customers in principle did not need to bother about any functionality related to the transmission, channel, RF settings, etcetera. When properly set, only the desired channel must be sent to a NIM, the mother board system only taking care of conditional access, MPEG decoding, demultiplexing and conversion to the output interface format.

- All front end related control loops are contained within the NIM: AFC, AGC, clock synchronisation. It also allows sharing of resources like the 4MHz crystal.

- It avoids most sensitive analogue interfaces, reducing the interfacing to I2C for control and MPEG2 TS as output. (In most channel decoders the TS was available both in serial and parallel format).

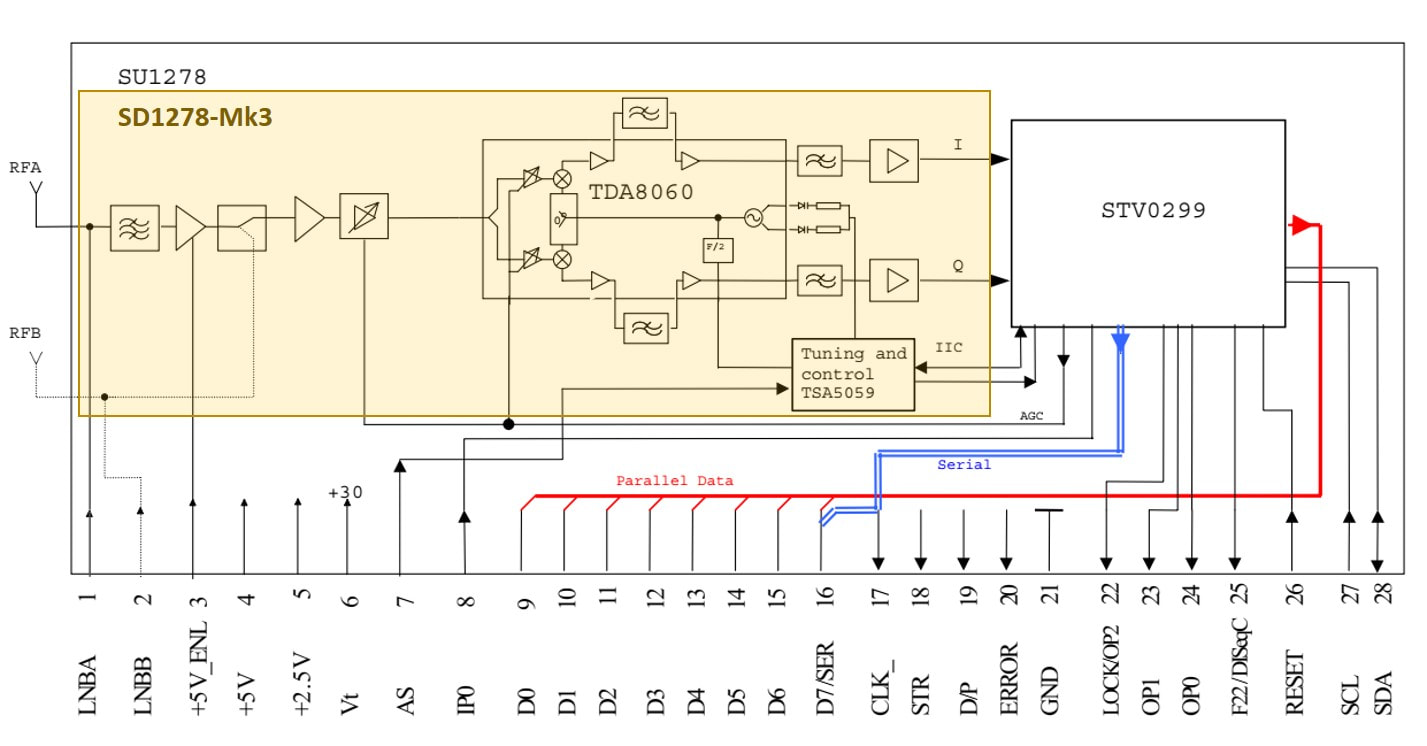

Block diagram of the Philips SU1278 satellite NIM. The yellow section is functionally identical to the SD1278-Mk3 front end. [Philisp SU1278 Data Sheet, August 2001]

|

The first satellite NIMs by the BU were based on the 1500 frame, but these were clearly too large (or too early) and it was decided, also because most customers were in the PC-card and STB domain, to switch to the short - 67mm - 1200 frame, although adapted to the mixed technology. The front end sections were copied 1:1 from the SD1278-Mk3, using the TDA8060 ZIF-MO and low phase noise TSA5059 PLL. This gave the SU1278 a range of 1-45MSymbols/s, since all Nyquist filtering was done digitally in the channel decoder.

|

As channel decoder the ST STV0299 was selected, which was becoming the dominant IC in the market. Philips Semiconductors was also active but suffered from the integration with VLSI in 1999. With that came a design centre in Rennes, France, from the former company Comatlas which was acquired earlier by VLSI and had a larger portfolio of channel decoders than Philips. It was decided that all channel decoder development would be concentrated in Rennes, but the usual internal politics delayed the process. It therefore took a while until the original VLSI VES1993 and Philips TDA10085 had merged into the new TDA10086. Which turned out to be a good IC, quite successful in the market, but too late for the SU1278. And thus the ST IC was selected. Apart from offering the by now standard variable rate QPSK channel decoding, with two on-board ADCs, it featured additionally:

- the STV0299 acted as I2C repeater for the tuner section. Because the low phase noise PLL was very sensitive to I2C crosstalk, it should be disconnected from the main I2C bus when stabilized. The I2C bus was therefore routed through the channel decoder, which would disconnect the output during normal operation. Only when a different channel had to be selected the bus would be made available to the PLL.

- the STV0299 contained a DiSEqC signal generator for control of the LNB, the details of which will be explained in the next LNB section.

- the PLL and channel decoder shared the same 4MHz crystal.

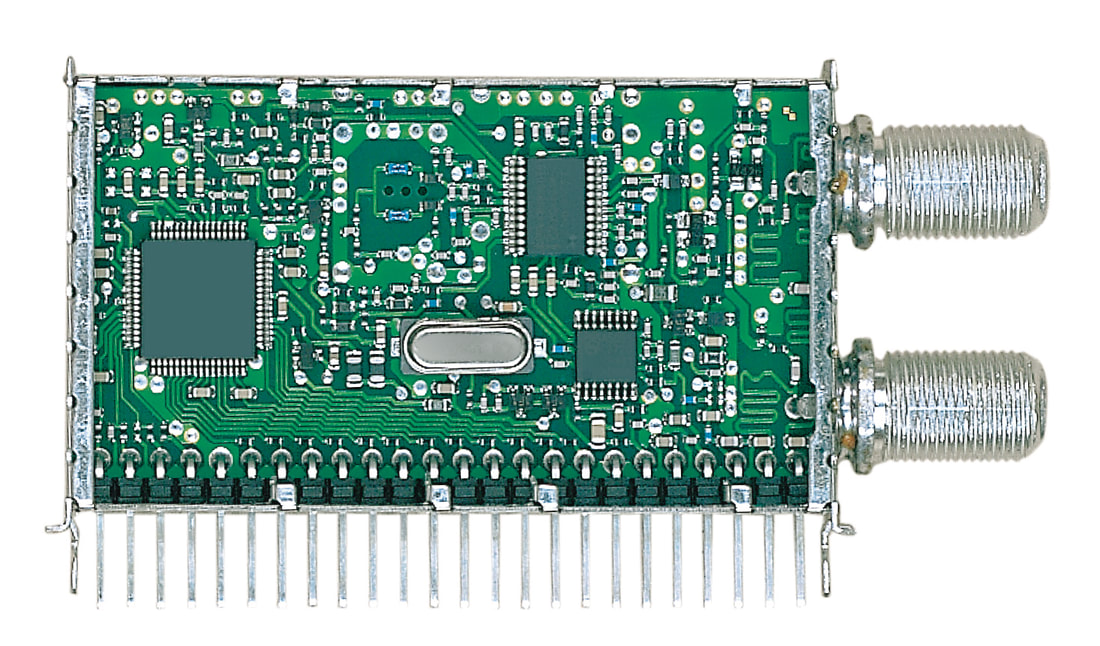

Unfortunately, I have no pictures of the Philips SU1278 interior. The picture shown her is NOT the final product, only a prototype, although the circuit lay out probably comes close to the final design. The main differences are the lack of internal frame screens, while this prototype has only 24 pins. The final product had 28. [via Darko Jancin]

|

The Philips SU1278/SHA on a typical PCI-card application. Note that the total solution has reduced to the NIM and the Philips SAA7146, the extremely successful MPEG2 decoder/demux.

|

With the departure of president Boonstra the company finally got rid of the "Let's make things better" slogan, still used on the SU1278-Mk1 leaflet on the left. The new company style omitted a slogan, but now made mandatory the use of happy boys and girls, pictured while enjoying - supposedly - the Philips products. All references to application domains, like the satellite dishes, were omitted.

|

The SU1278, introduced in 2001, did reasonably well in the market, given that a NIM was integrally an expensive module in the cost driven satellite market. The advantages were evident, though, and it saw immediate design in on PCI computer cards. However, two trends again put pressure on this product:

|

|

Integration of the ZIF MO and a PLL was the obvious next integration step, and multiple companies were working on it, including Philips Semiconductors with the TDA8260. However, that development ran into serious troubles, essentially due to the conservatism of the BL in Caen which stayed as much as possible in the HS5 bipolar-only node. But such a 16GHz fT node was by now quite outdated, and the design of a 4,5GHz oscillator with such limited frequency margin was really a stretch. In other words, the IC did not meet its specifications, and redesign in Qubic3 (32GHz fT) only started end 2002. Although that eventually turned out to be a good IC it came much too late to the market. In the meantime, a different solution was used, the TUA6100.